GCC Sukuk: A Primer, 3rd Edition

Investment Characteristics of US Dollar-Denominated Sukuk Originating from the Gulf Cooperation Council

We are delighted to release the third edition of our GCC Sukuk Primer. This white paper examines the investment landscape and characteristics of sukuk, or Islamic-compliant investment certificates.

We will cover the risk and return attributes of sukuk and explore their relationship to changes in the price of oil, as hydrocarbon prices have a large influence on the economies of Middle Eastern countries. There is limited global research on sukuk, so we will focus on those issued in Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE). Together, these six countries form the Gulf Cooperation Council (GCC), which has consistently led other countries in the issuance of US dollar-denominated sukuk. See the What is the GCC? subsection for more details.

The emerging market fixed-income communities of the GCC region are notable for their performance, relative stability, and development of their capital markets. The population of the GCC as of year-end 2022 was over 56 million, representing just 0.7% of the global population. The countries of the GCC generate 2.2% of global gross domestic product (GDP). However, 32.8% the world's oil supply comes from the GCC region, which gives these countries significant influence on the world stage.

The GCC Sukuk Primer is an extensive research report detailing the US dollar-denominated sukuk market. This report is divided into seven sections and two subsections to provide readers with a comprehensive overview of this emerging asset class.

Primary Sections include:

- The Dawn of the Golden Era: An Introduction

- Market Issuance & Trends: Sukuk Issuance Trends from 2011 to 2023

- History of GCC's Entry into the Fixed-Income Markets

- What's the Appeal for Investors?: What makes GCC fixed-income securities appealing to foreign investors. We characteristically coin this section as "plenty in the bank, plenty in the tank" to relay the region's substantively robust financial metrics and high investment-grade credit ratings of most issuers.

- The Price of Oil and the Sukuk Market - Understanding the Relationship: Understanding the relationship of price movements of oil and the sukuk market. This section includes details on the unique structuring of Islamic-compliant securities relative to conventional fixed-income bonds.

- Correlation characteristics of sukuk relative to other asset classes

- Putting a Pin in Relative Risk and Return: A detailed analysis of the risk and return characteristics of US dollar-denominated sukuk.

The two Subsections address:

- What is the GCC?: What is the Gulf Cooperation Council (GCC)

- JPMorgan's Inclusion of the GCC in its emerging market benchmarks; adoption and acceptance of an emerging region

The Dawn of the Golden Era

Since the second edition of this primer was published two years ago, the GCC was largely spared the hardships faced by the rest of the world, (particularly developed economies), such as historically high inflationary pressures, growing fiscal deficits, and ballooning of sovereign debt. Over this period, the GCC has experienced an economic renaissance that could be described as a "golden era."

This view is shared by others such as Viswas Raghaven, chief executive officer for JPMorgan Chase & Co. in Europe, the Middle East, and Africa. "You're seeing a real kind of swagger as countries like Saudi Arabia, UAE, Qatar, all are pretty well positioned, both for attracting money managers, hedge funds, to also their own domestic economies becoming mainstream," said Raghaven. "This is a golden era for Middle Eastern companies and in general, the Middle East. I think that it's here to stay."1

Raghaven's statement may have some merit. The GCC region demonstrated enviable financial growth in 2022 and 2023. At year-end 2022, Saudi Arabia posted a GDP growth rate of 8.7%, the highest GDP growth rate of any G20 economy, and broke the $1 trillion mark in economic value for the first time ever.2, 3 In 2022, real GDP growth for the entire GCC region was 7.9%, oil GDP growth was 12.1%, and non-oil GDP growth was 5.3%. For 2023 and 2024, real GDP growth in the GCC is estimated at 1.5% and 3.7%4, respectively. Global growth is projected to slow from 3.5% in 2022 to 3.0% in 2023 and 2.9% in 2024, well below the historical average of 3.8% for 2000 through 2019. The average growth rate of advanced economies is expected to slow down as well, starting at 2.6% in 2022, then lowering to 1.5% in 2023 and 1.4% in 2024.5

In October 2021, the International Monetary Fund (IMF) predicted in their Regional Economic Outlook that oil exporters such as the countries of the GCC were likely to see a cumulative windfall of $1 trillion between 2022 and 2026.6 The price of oil, as measured by West Texas Intermediate (WTI), averaged $85.95 per barrel over the two-year period, from 2022 through 2023. Over that same period, the GCC region's sovereign wealth funds grew an average of 20%, reaching about $4 trillion.7

While the GCC region's economic and financial numbers are impressive, several of its member-states have gained global prominence in other ways. Dubai hosted the 2021 World's Fair, Qatar hosted the 2022 FIFA World Cup, and the 28th annual United Nations Climate Change Conference took place in Dubai in November 2023.

The UAE has become a place of refuge for those adversely affected by the COVID-19 pandemic and geopolitical conflicts. Bloomberg's Covid Resilience Ranking, which ranks 53 countries based on 12 indicators including health care quality, virus mortality, and reopening travel, ranked the UAE as number one for its high vaccination rates and low infection rates.8 About 25,000 Ukrainians have relocated to the UAE to avoid the Russian-Ukrainian war.9 Russian citizens have sought sanctuary in the UAE as well; an estimated half a million Russians have been granted the right to live in the UAE as of February 2022.10

The population influx to the UAE was a boon to the country's real estate market.11 Property transactions surged along with valuations. By year-end 2022, total residential property transactions in the UAE exceeded 92,000 units, valued over AED 225 billion ($61.3 billion), a marked increase since 2018 when the country recorded less than 30,000 transactions, valued at near AED 75 billion ($20.4 billion). In the first three quarters of 2023, 87,000 homes were sold across the UAE, worth AED 222.7 billion.12 Luxury residential property sales also flourished, setting new records. The most expensive apartment unit sale in Dubai occurred in February 2023, valued at AED 410 million ($112 million).13

With the rapid growth in population, the UAE began establishing comprehensive urban master plans. The Dubai 2040 Urban Master Plan, initiated by Sheikh Mohammed bin Rashid Al Maktoum in March 2021, aims to increase the city's population from its current size of 3.3 million to an impressive 7.8 million by the year 2040.14 The region is determined to leverage its hydrocarbon riches by developing top-notch sectors and industries capable of drawing global commerce and trade opportunities.

The costs of development projects in the GCC, particularly for infrastructure, are simply staggering with estimates valued over $2 trillion. Saudi Arabia alone will require more than 800 million tons of cement to achieve its project plans by 2030, along with hiring over one million additional laborers and one hundred thousand engineers. As of November 21, 2023, over $178 billion in contracts had been awarded in the GCC in just one year. While a large number of these projects are related to the Energy sector, the largest single non-hydrocarbons deal was the $2.1 billion contract to build the Wynn gaming resort in Ras al-Khaimah.15

While infrastructure development projects in the GCC might not make the headlines, the GCC's entry into sports (soccer and golf in particular) has attracted considerable attention and controversy. As part of Saudi Arabia's Vison 2030 program, which is a national effort to move the country's economy away from its dependence on hydrocarbons, the government is expanding upon tourism, entertainment, and sports as a means of diversification. Saudi Arabia launched its National Tourism Strategy to foster the sector's development, create one million new jobs, and increase its contribution to GDP from the current 3.8% to 10% by 2030.16 The government had originally set a goal to attract 100 million visitors to Saudi Arabia by 2030, but in September of 2023, the target was raised to 150 million visitors. The original target was "no longer sufficient," said Mahmoud Abdulhadi, the Deputy Minister of Destination Enablement at the Ministry of Tourism.17

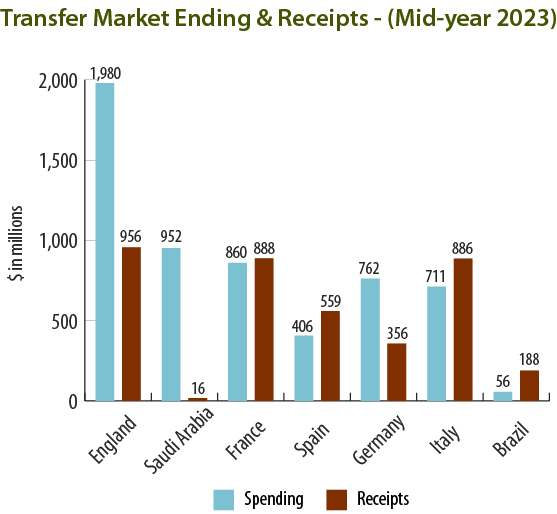

During the 2023 summer transfer window for soccer, the government of Saudi Arabia spent an equivalent of USD$952 million to attract top athletes to build the Saudi Pro League. The Premier League in England was the only other "big five" league to spend more than Saudi Arabia, at USD$1.39 billion.

Saudi Arabia has also entered the professional golf world. In June of 2022, LIV Golf had its first tournament, financed with $2 billion courtesy of the Public Investment Fund, sparking a rivalry with the Professional Golfers' Association (PGA). Soon the PGA and LIV embarked upon an ugly feud in the Western media and American courts. The battle ended in June 2023 with a surprising announcement; the two parties agreed to merge forces.18, 19

Critics have labeled Saudi Arabia's deployment of exorbitant financial resources as "sports washing." This term implies that Saudi Arabia's spending on sports and entertainment is an attempt to divert attention away from alleged controversies or perceived issues associated with governance structures.20

Market Issuance & Trends

The global sukuk market is made of diverse regionalized markets that each have their own unique attributes and characteristics. From year-end 2000 through year-end 2022, 61.4% of global sukuk issuance originated in Asian countries. The GCC and the Middle East issued 24.5% of the market share for the same period. The countries of Malaysia, Saudi Arabia, and Indonesia were the largest issuers, with market shares of 48.4%, 12.6% and 9.5%, respectively.22International sukuk issuance denominated in the US dollar represented 23.3% of overall global market share.23

As of writing, sukuk have been issued in 27 different currencies from around the world. By year-end 2023, the total volume of outstanding global sukuk was over $850 billion, exceeding the size of the eurodollar's high yield market by nearly $100 billion.24 Malaysian ringgit has the largest share of the market, representing 47% of global issuance from year-end 2000 through year-end 2022. US dollar-denominated sukuk is the next largest group, representing 22% of global issuance, and Saudi Arabian riyal-denominated sukuk represents 10%. In recent years, local currency markets have developed in size and issuance. For 2022, Malaysian ringgit represented 36.8%, Saudi Arabian riyal represented 20.9%, the US dollar represented 19.6%, the Indonesian rupee represented 9.9%, and the Qatari riyal represented 4.5% of global sukuk issuance.25

| Year | Total Outstanding ($bn) | % Chg in Market | USD Outstanding ($bn) | USD as % of Outstanding |

| YE 2017 | 444.25 | 16.8% | 122.28 | 27.5% |

| YE 2018 | 481.63 | 8.4% | 128.74 | 26.7% |

| YE 2019 | 544.47 | 13.0% | 142.09 | 26.1% |

| YE 2020 | 630.13 | 15.7% | 165.84 | 26.3% |

| YE 2021 | 711.17 | 12.9% | 183.36 | 25.8% |

| YE 2022 | 765.42 | 7.6% | 183.96 | 24.0% |

| YE 2023 | 848.46 | 10.8% | 211.96 | 25.0% |

There are typically four classifications of sukuk issuance: sovereign, quasi-sovereign, corporate, and financial issues. As of year-end 2022, total international sukuk outstanding by issuer category was led by sovereigns at 45% of the market, followed by quasi-sovereigns at 21%, financial issues at 19%, and corporates at 15%.26 Quasi-sovereigns represented 39.9% of international sukuk issued in calendar 2022, followed by sovereign issuers at 29.7%, corporates at 15.8%, and financial issues at 14.6%.27

| Year-End 2023 | |||||

| $ Amt (bn) 848.46 | % of total $ | Count 4,195 | 848,460,000,000 | ||

| Malaysian ringgit | MYR | 312.83 | 36.9% | 2,845 | 312,830,000,000 |

| US dollar | USD | 211.98 | 25.0% | 355 | 211,980,000,000 |

| Saudi riyal | SAR | 173.57 | 20.5% | 214 | 173,570,000,000 |

| Indonesian rupee | IDR | 87.16 | 10.3% | 335 | 87,160,000,000 |

| Pakistani rupee | PAK | 19.38 | 2.3% | 47 | 19,380,000,000 |

| Turkish lira | TRY | 13.90 | 1.6% | 219 | 13,900,000,000 |

| Qatari riyal | QAR | 8.94 | 1.1% | 18 | 8,940,000,000 |

| UAE dirham | AED | 4.49 | 0.5% | 8 | 4,490,000,000 |

| 832.25 | 98.1% | 4,041 | 832,250,000,000 |

At the end of 2023, there was a rapid increase in the size of the overall sukuk market across all currencies. Global issuance was $848.45 billion, a 10.8% year-over-year increase, slightly above its three-year compound annual growth rate (CAGR) of 10.4%. Malaysian ringgit had the largest representation of the market share at 36.9%, followed by the US dollar at 25.0%, and the Saudi Arabian riyal at 20.5%.

US Dollar Issuance Trends – Introducing GCC's Dominance

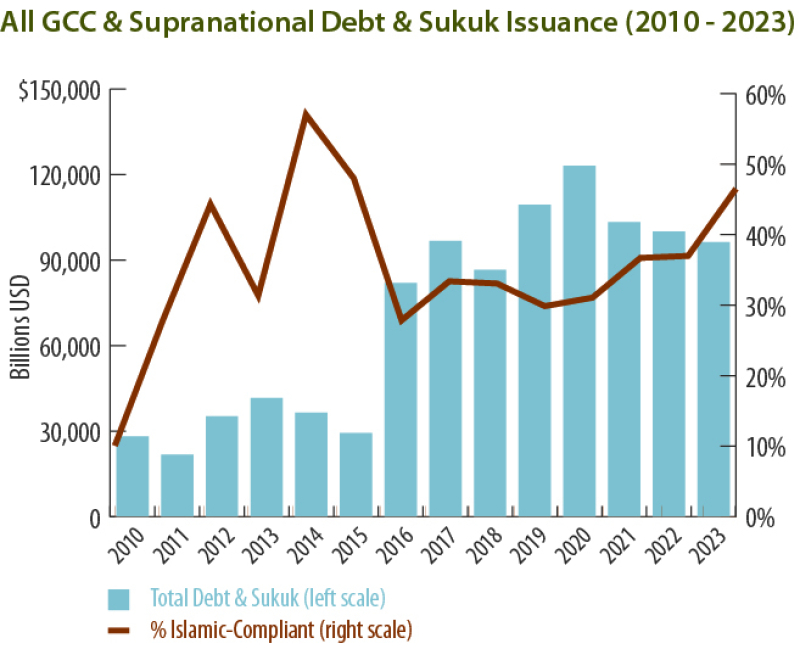

For the five-year period ended 2023, the GCC's market share of issuance in US dollar-denominated sukuk averaged 45.4%. For the five-year period ended 2022, that average was 48%. While Malaysia retained its title as the largest sukukissuer though its local currency, the country's share of US dollar-denominated issues was just 2.9%.

At year-end 2023, total issuance of US dollar-denominated sukuk was $58.1 billion, reflecting a 55.9% year-over-year increase and significantly above its three-year CAGR of 8.6%. The substantial uptick in sukuk issuance in 2023 offset the large decline in issuance in 2022. This decline was due to higher oil prices, which averaged $94.26 per barrel in 2022 and reached a high of $130.50 on March 7, 2022. Total issuance of US dollar-denominated sukuk in 2022 was $37.2 billion, down -24.5% since year-end 2021 when issuance was $49.4 billion.

The GCC region represented 54.5% of global sukuk issuance in 2023, above its three-year average of 41.9% which was skewed because GCC issuance had low representation in 2022 of 28.1%. Supranational entities were the second largest issuer in 2023 at 27.1% of total issuance, down from its three-year average of 36.8%. The third largest issuer was Turkey at 5.9% and the fourth largest issuer was Indonesia at 3.7%.

| US Dollar Sukuk Issuance Trends (2010 - 2023) | |||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

| Total Islamic Issuance ($ bn) | 9,415 | 18,536 | 18,450 | 28,560 | 21,093 | 32,435 | 38,783 | 33,846 | 38,724 | 45,291 | 49,364 | 37,249 | 58,084 |

| Change in % | 96.9% | -0.5% | 54.8% | -26.1% | 53.8% | 19.6% | -12.7% | 14.4% | 17.0% | 9.0% | -24.5% | 55.9% | |

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

| Region of Issuance | |||||||||||||

| GCC Issues | 56.5% | 75.8% | 61.0% | 36.7% | 28.5% | 35.1% | 49.5% | 51.4% | 52.8% | 48.8% | 43.0% | 28.1% | 54.5% |

| Supranationals | 8.0% | 8.6% | 14.5% | 36.4% | 38.9% | 35.3% | 33.7% | 33.2% | 32.4% | 36.9% | 38.3% | 44.9% | 27.1% |

| Malaysia | 21.2% | 1.9% | 4.3% | 2.8% | 17.2% | 11.5% | 0.3% | 3.2% | 1.3% | 1.1% | 4.9% | 0.0% | 2.9% |

| Indonesia | 10.6% | 5.4% | 8.1% | 5.3% | 9.5% | 7.7% | 7.7% | 9.2% | 5.4% | 5.5% | 6.1% | 9.4% | 3.7% |

| Turkey | 3.7% | 8.1% | 11.9% | 8.2% | 1.2% | 5.7% | 3.5% | 1.5% | 5.8% | 5.5% | 6.2% | 14.8% | 5.9% |

| Pakistan | 0.0% | 0.0% | 0.0% | 3.5% | 0.0% | 3.1% | 2.6% | 0.0% | 0.0% | 0.0% | 0.0% | 2.7% | 0.0% |

| Hong Kong | 0.0% | 0.0% | 0.0% | 3.5% | 4.7% | 1.2% | 2.6% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

| Europe | 0.0% | 0.2% | 0.1% | 0.1% | 0.0% | 0.3% | 0.0% | 1.6% | 2.4% | 2.2% | 0.5% | 0.1% | 0.6% |

| Maldives | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 1.0% | 0.0% | 0.0% |

| Egypt | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 2.6% |

| India | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.1% | 0.0% |

| Philippines | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 1.7% |

| United States | 0.0% | 0.0% | 0.0% | 1.8% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 1.0% |

| South Africa | 0.0% | 0.0% | 0.0% | 1.8% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

| Total | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| Regionalized Sumary | |||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

| GCC | 56.5% | 75.8% | 61.0% | 36.7% | 28.5% | 35.1% | 49.5% | 51.4% | 52.8% | 48.8% | 43.0% | 28.1% | 54.5% |

| Supranational | 8.0% | 8.6% | 14.5% | 36.4% | 38.9% | 35.3% | 33.7% | 33.2% | 32.4% | 36.9% | 38.3% | 44.9% | 27.1% |

| Asia (Includes Pakistan, India, & Maldives) | 31.9% | 7.3% | 12.5% | 15.1% | 31.4% | 23.5% | 13.2% | 12.3% | 6.7% | 6.6% | 12.0% | 12.2% | 8.3% |

| MENA excluding GCC members | 3.7% | 8.1% | 11.9% | 8.2% | 1.2% | 5.7% | 3.5% | 1.5% | 5.8% | 5.5% | 6.2% | 14.8% | 8.5% |

| Europe | 0.0% | 0.2% | 0.1% | 0.1% | 0.0% | 0.3% | 0.0% | 1.6% | 2.4% | 2.2% | 0.5% | 0.1% | 0.6% |

| Other | 0.0% | 0.0% | 0.0% | 3.5% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 1.0% |

| Total | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| GCC & Supranational (only) | 64.4% | 84.4% | 75.5% | 73.1% | 67.4% | 70.4% | 83.3% | 84.6% | 85.1% | 85.7% | 81.2% | 73.0% | 81.6% |

History of GCC's Entry into the Fixed-Income Markets

Broadly speaking, the six member-states of the GCC were not active issuers of debt or sukuk before 2016. When oil prices collapsed from 2014 through 2016, the GCC turned to the capital markets to supplement their gaps in government funding. The price of oil dropped from a high of $107.26 per barrel on June 20, 2014, to a low of $26.21 on February 11, 2015 — a 75.6% decrease! It would be another 15 months before the price of oil rose above $50.00 per barrel, on October 6, 2016.

The rapid decline of hydrocarbon revenues placed each of the GCC members in a difficult fiscal position. They began dipping into their regional pools of savings (including sovereign wealth funds) to offset fiscal shortfalls. In 2015, Saudi Arabia consumed an estimated $115 billion of its sovereign wealth fund's reserves, left with a projected balance of $600 billion in early 2016. If oil remained below $40 per barrel in 2017, Saudi Arabia would have had to draw down another $150 to $200 billion.33 It was entirely plausible that Saudi Arabia could burn through its entire sovereign wealth fund in a matter of a few years.

In April of 2016, Abu Dhabi issued a $5 billion bond to help offset a projected $10 billion deficit. It was the UAE's first bond sale in seven years since issuing a $1.5 billion note in April 2009.34, 35 The high investment-grade bond was in such strong demand that investors placed over 600 orders for it, exceeding $17 billion.36 Other GCC members took notice of Abu Dhabi's success, realizing that external investors could indeed help offset budgetary shortfalls. The GCC began to consider these investors as a primary source to fund other capital development and infrastructure projects; later, regional banks and non-financial corporate issuers came to the market for funding.

When GCC members entered the market, their timing was fortuitous for market participants, particularly those seeking Islamic-compliant securities. Malaysia's central bank, Bank Negara Malaysia, stopped issuing US dollar-denominated sukuk in summer 2015, and sukuk issuance declined by -42.5% in the second half of the year.37

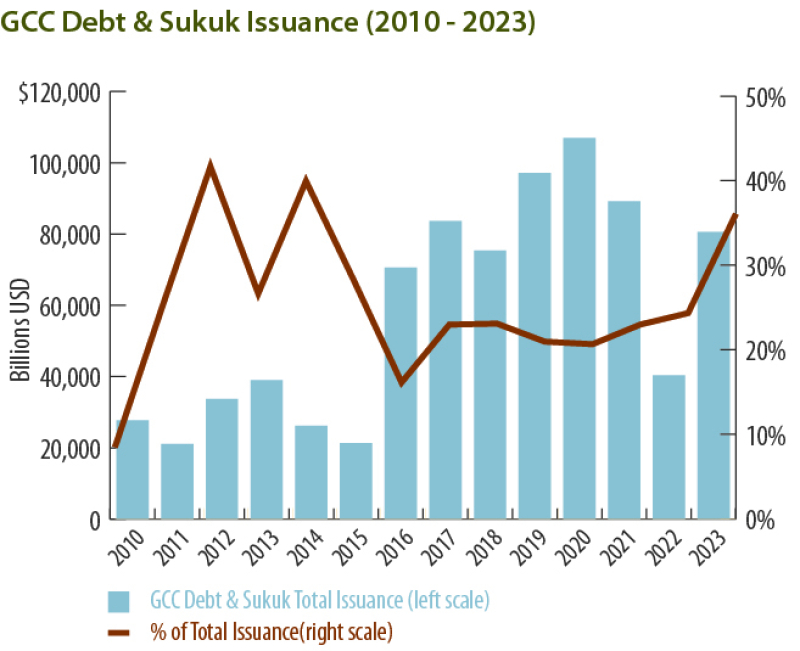

The GCC region, including supranationals, is an active issuer of both conventional debt and sukuk. For the full 2023 calendar year, the GCC issued $96.3 billion in conventional debt and sukuk, a decrease of -3.7% in 2022, and a three-year CAGR of -7.8%. For just sukuk in 2023, the GCC issued $44.8 billion, a year-over-year increase of 21.1%, above its three-year CAGR of 5.4%. Islamic-compliant securities represented 46.5% of fixed-income issuance from the GCC region, above its three-year average of 40.1%. Excluding Islamic-compliant supranationals such as the Islamic Development Bank (headquartered in Jeddah, Saudi Arabia), sukuk represented 36.1% of security issuance in 2023, also above its three-year average of 27.8%. From year-end 2009 through year-end 2023, the GCC's total issuance of both conventional bonds and sukuk was $990.8 billion.

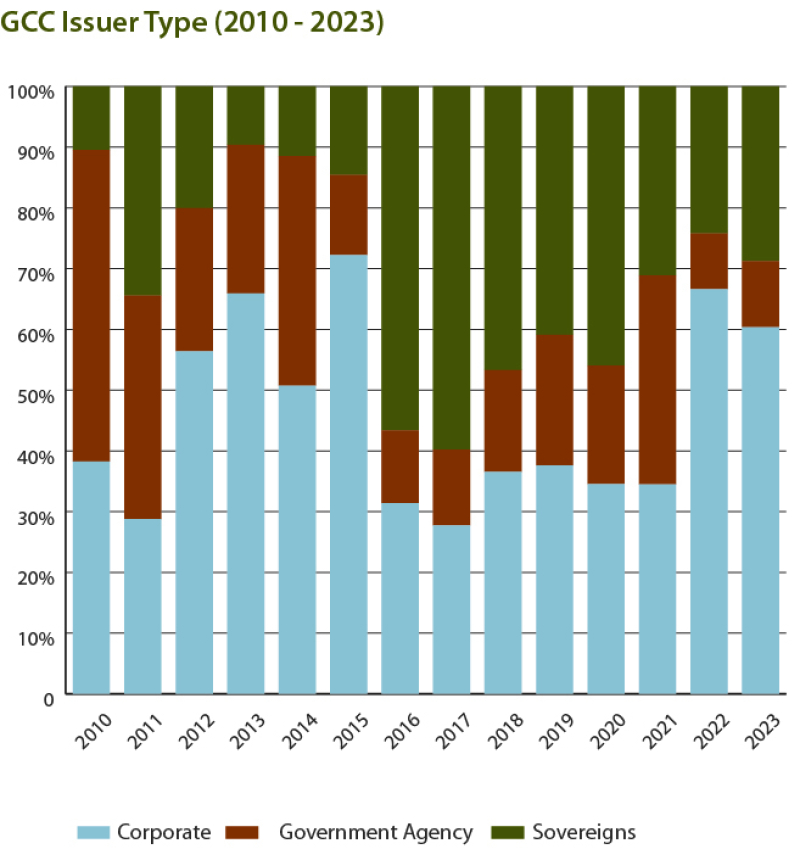

If we exclude supranationals when examining GCC issuance trends of sukuk, the issuer types include sovereign, government agencies, and corporates. Sovereign sukuk represented 60.4% of securities issued in 2023, down from 66.6% issued in 2022. Corporate sukuk issuance was 28.8%, up from 24.2% the year before. Sukuk issued by government agencies comprised 10.9%, up from 9.2% the year before. The three-year averages of sovereign, corporate, and government agency issues was 53.8%, 28.0%, and 18.1%, respectively.

Qualified proceeds use sukuk, or ESG sukuk, is gaining traction among investors. Indonesia issued its first sovereign green sukuk in March of 2018 at $1.5 billion. In 2019, Majid al Futtaim issued the first corporate US dollar-denominated sukukwith a $600 million offering. Since then, ESG sukuk extended beyond green issues to include sustainable sukuk and sustainability linked sukuk. In 2023, $7.2 billion in ESG sukuk were issued, a year-over-year increase of 54.8%. The GCC issued $6.2 billion in ESG sukuk in 2023, representing 86.1% of the market.

| US Dollar-Denominated Qualified Proceeds Use Sukuk | |||||||

| All Qualified Proceeds Use Sukuk ($bn) | All Qualified Proceeds Use Sukuk from GCC ($bn) | GCC as % | Green Sukuk ($bn) | Sustainable Sukuk ($bn) | Sustainability-Linked Sukuk ($bn) | ||

| 2023 | 7,200 | 6,200 | 86.1% | 5,200 | 2,000 | - | |

| 2022 | 4,650 | 3,150 | 67.7% | 2,400 | 2,250 | - | |

| 2021 | 4,900 | 2,500 | 51.0% | 750 | 3,350 | 800 | |

| 2020 | 4,150 | 3,400 | 81.9% | 2,050 | 1,500 | 600 | |

| 2019 | 1,950 | 1,200 | 61.5% | 1,950 | - | - | |

| 2018 | 1,250 | - | 0.0% | 1,250 | - | - | |

| Total | 24,100 | 16,450 | |||||

| Source: Bloomberg | |||||||

What's the Appeal for Investors?

The GCC region offers investors unique investment attributes and characteristics that are typically uncommon among most emerging and developing world fixed-income markets – namely, favorable risk-adjusted returns and stability. In fact, the GCC region offers investors among the highest risk-adjusted returns when compared to developed and emerging/developing fixed-income markets.

In general terms, there are six primary factors that can help explain the regions' favorable risk-adjusted returns and overall stability. These include: (1) favorable yield enhancement to developed economies, (2) strong credit ratings, (3) low debt metrics, (4) fixed currency peg to the US dollar, (5) robust capital buffers, and (6) enormous hydrocarbon reserves. To simplify, we often characterized the regions' investment attributes with the following short tag line, "plenty in the bank and plenty in the tank." We'll explain this in greater detail later in the report.

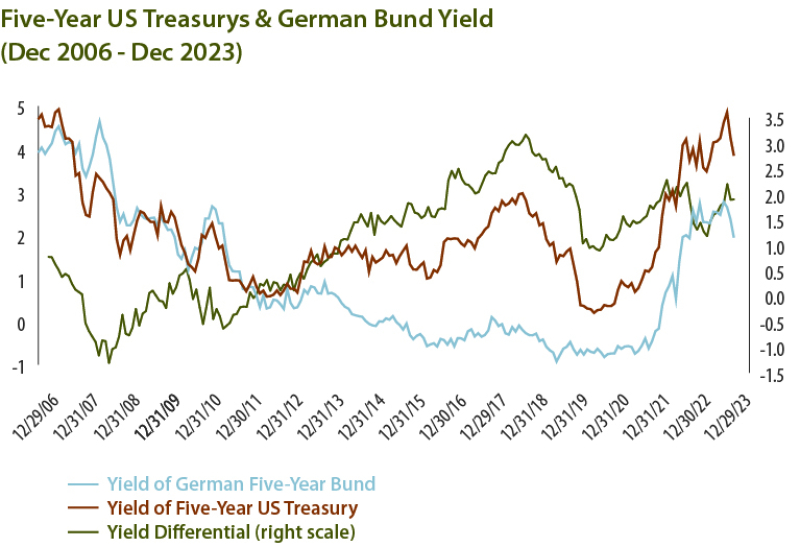

Issues from the GCC region offer favorable yield enhancement relative to developed world government bonds. The Global Financial Crisis (GFC) led to an extended period of low interest rates and low to negative yields. The low interest rate regime was detrimental to many institutions that needed to meet future funding obligations, such as pension funds. This period was referred to as a "yield famine."

In the graph "Five-Year US Treasurys & German Bund Yield (Dec 2006-Dec 2023)," note the movement of the yields after September 15, 2008 – the pivotal date that marks the beginning of the GFC, when the US government allowed the investment bank Lehman Brothers to go bankrupt.38 In January 2015, the yield of the five-year German Bund entered into negative territory at -0.048%, later falling to -0.923% by month-end of August 2019. The five-year US Treasury yield hit a low of 0.205% in July 2020.

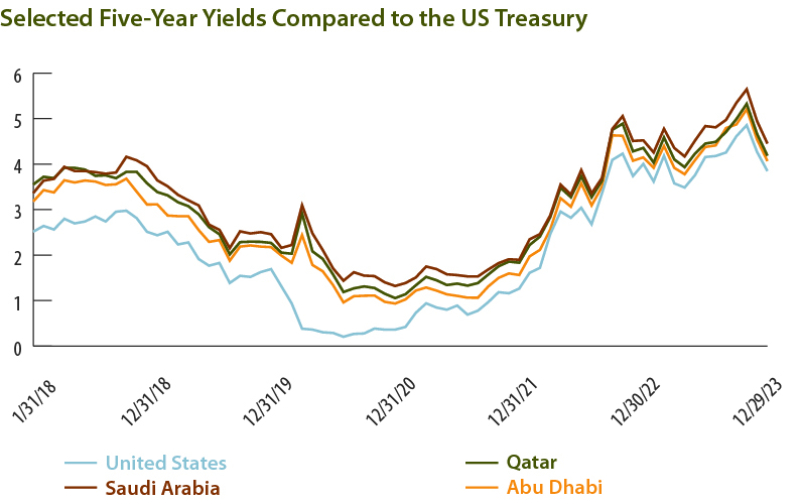

For institutional investors seeking issues with high investment-grade credit ratings, the GCC offered a solution, in part, to the low-yield environment. As shown in "Selected Five-Year Yields Compared to the US Treasury," Abu Dhabi, Qatar, and the Kingdom of Saudi Arabia provided favorable yields above the five-year US Treasury. Yield spreads materially compressed in recent years. For Qatar and Abu Dhabi, yield spreads compressed by over 60% between 2018 and 2023. For the two-year period ended 2019, Saudi Arabia, Qatar, and Abu Dhabi offered average yield enhancements of 102-bps, 90-bps, and 66-bps above the five-year US Treasury, respectively. The marked tightening in yield spreads can be seen for the two-year period ended 2023. Saudi Arabia, Qatar, and Abu Dhabi each had an average yield enhancement of 66-bps, 47-bps, and 31-bps above the five-year Treasury, respectively.

The tighter spreads can be attributed to strong sovereign fiscal metrics, stable high grade credit ratings, and high hydrocarbon prices. These countries also worked hard to develop favorable rapport with institutional investors, which helped provide stability over time.

| Average Yield Enhancement Above Five-Year US Treasury (expressed in yield, bps) | |||

| Year | KSA | Qatar | Abu Dhabi |

| 2023 | 0.691 | 0.409 | 0.298 |

| 2022 | 0.636 | 0.535 | 0.325 |

| 2021 | 0.764 | 0.601 | 0.368 |

| 2020 | 1.433 | 1.198 | 0.980 |

| 2019 | 0.948 | 0.777 | 0.564 |

| 2018 | 1.095 | 1.026 | 0.748 |

| Year | KSA | Qatar | Abu Dhabi |

| 2022 - 2023 | 0.66 | 0.47 | 0.31 |

| 2020 - 2021 | 1.1 | 0.90 | 0.67 |

| 2018 - 2019 | 1.02 | 0.90 | 0.66 |

| Yield Compression from 2018-2019 to 2022-2023 | |||

| KSA | Qatar | Abu Dhabi | |

| 36.9% | 60.1% | 60.2% | |

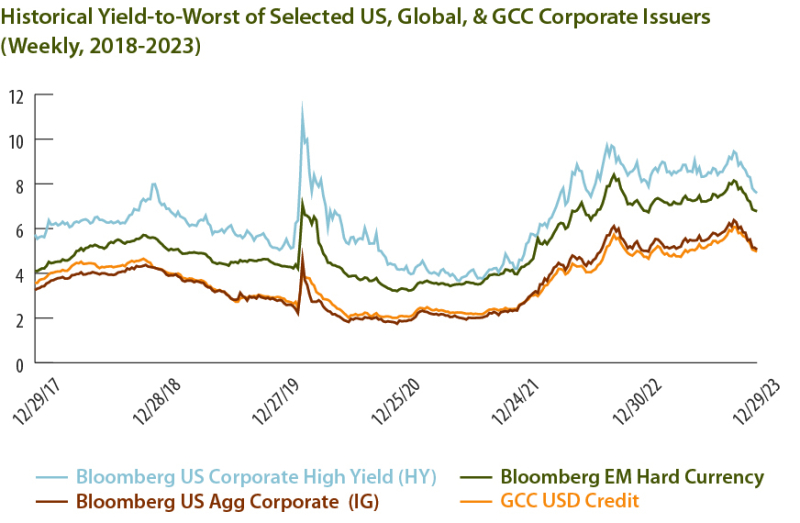

The yields of the benchmarks Bloomberg US Corporate High Yield Index, Bloomberg Emerging Market Hard Currency Index, Bloomberg US Aggregate Corporate Investment Grade Index, and Bloomberg GCC USD Credit Statistics Index incorporate both sovereign and corporate issuers. The indices demonstrate competitively low yield-to-worst (YTW) metrics relative to commonly known fixed-income indices that US investors use. The low yields of these benchmarks signal investor confidence in the region and heightened investor demand, which lowers their reported YTW.

Investors are also attracted to the GCC region because of the high investment-grade ratings of sovereign debt. Many of the member-states of the GCC retained credit ratings that are typically awarded only to developed countries. Fitch rated Abu Dhabi sovereign debt and sukuk credit "AA", followed by Qatar at "AA-," and Saudi Arabia at "A+." In comparison, Fitch rated the United States "AA+: stable" following their decision to downgrade the sovereign status from "AAA" back on August 1, 2023. The reason for Fitch's downgrade was the deteriorating sustainability of the US fiscal and debt profile in conjunction with its contentious political landscape when compared to other "AAA" issuers.39 Meanwhile, the United Kingdom was rated "AA-", Negative, and China was rated "A+, Stable."40, 41

While selected members of the GCC have achieved investment-grade credit ratings, the overall stability of their credit ratings over time are also worth examining.

| Saudi Arabia | Qatar | Abu Dhabi | ||||||||

| Fitch | Moody's | S&P | Fitch | Moody's | S&P | Fitch | Moody's | S&P | ||

| 2023 | A+, Stable | A1, Positive | A, Stable | AA-, Positive | Aa2 Stable | AA, Stable | AA, Stable | Aa2, Stable | AA, Stable | |

| 2022 | A-, Positive | Aa3 Stable | AA-, Stable | |||||||

| 2021 | A, Stable | A1, Stable | AA-, Stable | AA-, Stable | Aa2, Stable | |||||

| 2020 | A, Negative | A1, Negative | AA-, Stable | Aa3 Stable | NR | AA-, Stable | ||||

| 2019 | A, Stable | A1, Stable | AA, Negative | Aa3 Stable | AA-, NR | AA, Stable | Aa2, Stable | AA, Developing | ||

| 2018 | A+, Stable | A1, Stable | AA, Stable | Aa3 Stable | A, Stable | |||||

The GCC region has largely demonstrated resilient and stable credit ratings despite the price of oil experiencing material volatility over the last five years.

GCC's Indebtedness vs. the Developed World

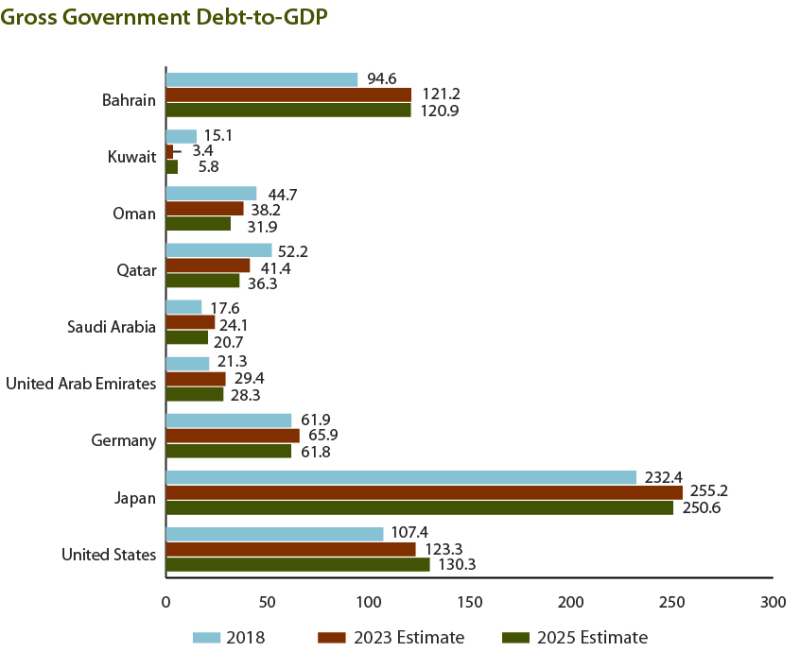

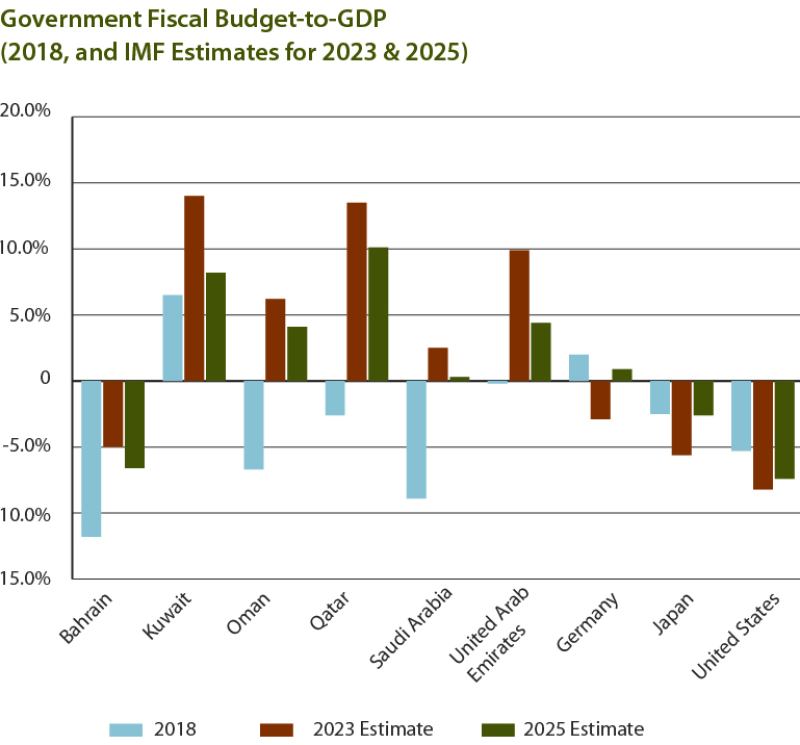

When Abu Dhabi issued debt in April 2016, it wasn't just the attractive yields and favorable "AA" credit rating status that tantalized investors; it was also the UAE's low outstanding debt. The debt-to-GDP ratio for the GCC countries (except for Bahrain and Oman, which retain below investment-grade credit profiles) is extremely low. Low debt affords a country greater financial flexibility to meet its ongoing financial debt and sukuk obligations compared to a highly leveraged country. Some of the GCC members retained high credit ratings in addition to extremely low levels of debt when compared to substantially leveraged developed countries. The selected periods (2018, 2023, and 2025) are meant to reflect each country's debt burden prior to the pandemic, post-pandemic, and anticipated projections several years after the pandemic.

| Gross Government Debt-to-GDP | Fiscal Budget Measured as a % of GDP | |||||||

| 2018 | 2023 Estimate | 2025 Estimate | 2018 | 2023 Estimate | 2025 Estimate | |||

| Bahrain | 94.6 | 121.2 | 120.9 | -11.8 | -5.0 | -6.6 | ||

| Kuwait | 15.1 | 3.4 | 5.8 | 6.5 | 14.0 | 8.2 | ||

| Oman | 44.7 | 38.2 | 31.9 | -6.7 | 6.2 | 4.1 | ||

| Qatar | 52.2 | 41.4 | 36.3 | -2.6 | 13.5 | 10.1 | ||

| Saudi Arabia | 17.6 | 24.1 | 20.7 | -8.9 | 2.5 | 0.3 | ||

| United Arab Emirates | 21.3 | 29.4 | 28.3 | -0.2 | 9.9 | 4.4 | ||

| Germany | 61.9 | 65.9 | 61.8 | 2 | -2.9 | 0.9 | ||

| Japan | 232.4 | 255.2 | 250.6 | -2.5 | -5.6 | -2.6 | ||

| United States | 107.4 | 123.3 | 130.3 | -5.3 | -8.2 | -7.4 | ||

Looking at Saudi Arabia and the UAE, we see a story of fiscal budgets reversing from deficits into surpluses. However, we note that the Kingdom of Saudi Arabia revised their own budget forecast for year-end 2023 to 0.4% of GDP on October 1, 2023, due to lower oil revenues.42

Another credit rating agency, Moody's, downgraded the US in November 2023 from "Stable" to "Negative" but retained its "AAA" rating. Moody's downgrading rationale echoed that of Fitch: rising debt sustainability risks, large fiscal spending, and a contentious political landscape inhibiting the parties from effectively addressing these issues.43

Plenty in the Bank and Plenty in the Tank

Even though each member-state in the GCC retains its own local currency, the region can be characterized as a US dollar-based economy. The origins of the US dollar's dominance and integration in the region can be credited, in part, to a signed agreement that took place on June 8, 1974, between Secretary of State Henry Kissinger and Saudi Prince Fahd. The agreement concerned economic and military cooperation between the two countries, but also formalized two important points for the US. First, oil would be priced and invoiced in US dollars. Second, the proceeds from the sale of oil would be invested in US Treasurys or other dollar-denominated securities.44 In June 1986, the Kingdom of Saudi Arabia pegged its local riyal to the US dollar at a fixed rate of 3.7500.45 This currency peg has remained in effect ever since.46

Later, other countries within the GCC began to peg their currency to the US dollar. In 1997, the UAE established a dollar-dirham peg of one US dollar to 3.6725 dirham.47 Kuwait is the one outlier, which employs a basket of currencies rather than peg their currency to the dollar. Even with this approach, Kuwait is largely a US dollar-centric economy.48

When a country has a US dollar-pegged currency, its government usually adjusts its monetary policies (such as the benchmark interest rate) in tandem with the US Federal Reserve's interest rate policies. If that country doesn't coordinate its monetary policy actions, its fixed-rate currency peg may be adversely affected, depreciating relative to the US dollar. GCC assets, government receipts, liabilities, and fiscal budgets become US dollar-denominated proxies, which helps them avoid currency mismatches — a situation where a country's assets are denominated in their local currency while having their liabilities and obligations payable in another currency. Foreign investors can find this attractive, as it helps them to potentially sidestep adverse currency devaluations on their investments.

Plenty in the Bank

In 1938, Saudi Arabia began commercial production from its first oil well, Damman No. 7, aptly nicknamed the "Prosperity Well."49 Over the following eight decades, Saudi Arabia and its fellow GCC members became major suppliers of the world's insatiable energy needs. In 2022, the GCC member-states satisfied 32.8% of the world's oil demand, with Saudi Arabia representing 12.9%, the UAE at 4.3% and Kuwait at 3.2%. The GCC region has amassed enormous wealth since that first oil well.

Eight of the GCC's sovereign wealth funds control 35.3%, or $3.7 trillion, of the total $10.6 trillion of assets held among the top 20 sovereign wealth funds.50 At year-end 2021, the population of the GCC region was estimated at 56.1 million.51However, about half of the region's population are expats, which reduces the "natural population" to around 27.6 million.52, 53 In no other region of the world is there such a large concentration of wealth among such a small population.

| Gross Government Debt-to-GDP | ||||

| Rank | Sovereign Wealth Fund | ($ trillions) | Country | Region |

| 1 | Norway Government Pension Fund Global | $1,478 | Norway | Europe |

| 2 | China Investment Corporation | $1,351 | China | Asia |

| 3 | SAFE Investment Company | $1,020 | China | Asia |

| 4 | Abu Dhabi Investment Authority | $853 | UAE | Middle East |

| 5 | Kuwait Investment Authority | $803 | Kuwait | Middle East |

| 6 | Public Investment Fund | $777 | Saudi Arabia | Middle East |

| 7 | GIC Private Limited | $770 | Singapore | Asia |

| 8 | Hong Kong Monetary Authority Investment Portfolio | $514 | Hong Kong | Asia |

| 9 | Temasek Holdings | $492 | Singapore | Asia |

| 10 | Qatar Investment Authority | $475 | Qatar | Middle East |

| 11 | National Council for Social Security Fund | $416 | China | Asia |

| 12 | Investment Corporation of Dubai | $320 | UAE | Middle East |

| 13 | Mubadala Investment Company | $287 | UAE | Middle East |

| 14 | Türkiye Varlık Fonu Yönetimi A.Ş. (Turkey Wealth Fund) | $279 | Turkey | Middle East |

| 15 | Korea Investment Corporation (KIC) | $169 | South Korea | Asia |

| 16 | Abu Dhabi Developmental Holding Company PJSC | $159 | UAE | Middle East |

| 17 | National Welfare Fund of the Russian Federation | $148 | Russia | Europe |

| 18 | Future Fund Management Agency | $132 | Australia | Asia |

| 19 | Alberta Investment Management Corporation (AIMCo) | $124 | Canada | North America |

| 20 | Emirates Investment Authority | $87 | UAE | Middle East |

| Total for TOP 20 SWF | $10,655 | |||

Not all the sovereign wealth of the GCC region is allocated for immediate use; some is dedicated for the future. Kuwait's Future Generations Fund, an intergenerational savings fund, permits no asset withdrawals unless sanctioned by law.54The only time that proceeds were withdrawn from the Fund was in conjunction with the 1990-91 Iraqi invasion and occupation. From 1990 through 1994, nearly $85 billion in assets were withdrawn to pay for the cost of liberation and subsequent reconstruction, and were later fully repaid.55 As Kuwait's deficit rose and the government and parliament refused to agree on a funding strategy, credit rating agency S&P downgraded the country's rating from "AA-" to "A+" with a negative outlook, which "primarily reflects risks relating to the government's ability to overcome the institutional roadblocks preventing it from implementing a financing strategy for future deficits."56 As the stalemate continued, Kuwait's lawmakers proposed legislation to tap assets from the Fund.57

Following the onset of the pandemic, oil prices steadily rose, reaching a high on March 7, 2022, at $130.50 a barrel. This rise helped the GCC region further improve its fiscal standing.

According to the IMF, high oil prices and low headline inflation are likely to make the Gulf economies an additional $1.4 trillion in revenue over the next four to five years.58 Bahrain and Oman, which are rated below-investment grade, were able to materially improve their fiscal budgets due to the added revenues. Between year-end 2021 and year-end 2022, Bahrain's fiscal deficit decreased by 85%, or 178 million dinars ($472 million), according to a preliminary financial estimate from the country's Finance Ministry.59 In Oman, the country's deficit was 1.55 billion rials ($4.03 billion) at year-end 2021. At year-end 2022, Oman projected a fiscal surplus of 1.15 billion rials ($2.98 billion).60 S&P Global Ratings upgraded Oman's credit rating first in December 2022, from "BB-" to "BB", and again in September 2023, from "BB" to "BB+" due to improved fiscal performance and lower public debt.61, 62 The fiscal health of corporate issuers in the region has improved. This oil-wealth effect also helped Kuwait to improve its outlook from "Negative" to "Stable" while retaining its "A+" rating.63

Plenty in the Tank

While the transition toward a low-hydrocarbon global economy is a high priority, it will take considerable time, particularly with the resurgence of geopolitical risks and movements by governments to prioritize national energy security. In October 2023, Italy, France, and the Netherlands each signed a liquefied natural gas (LNG) contract with Qatar through 2050.64, 65, 66 These agreements took place just before the United Nations Climate Change Conference in Dubai in November and December of 2023. One of the goals of the European Green Deal is for the EU to achieve carbon neutrality and net-zero GHG emissions by 2050. The agreements that Italy, France, and the Netherlands made with Qatar may challenge these goals.

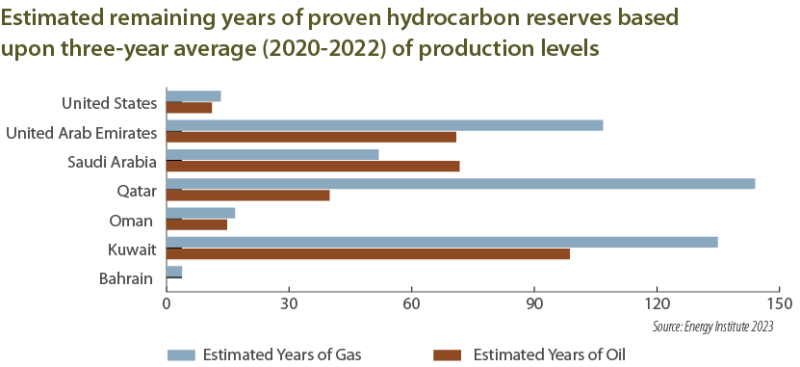

According to the Energy Institute, which compiles data on hydrocarbon reserves and production levels, the GCC region is rich in hydrocarbon reserves. The Energy Institute's most recent publication found that, based upon production rate three-year averages (2020-2022), Qatar, Kuwait, and Saudi Arabia each have well over 100 years of natural gas reserves, at 144, 135, and 107 years, respectively. As it relates to estimated proven oil reserves and three-year average production rates, Kuwait is projected to satiate demand for 99 years, with Saudi Arabia and the UAE each having over 70 years in reserves.

The GCC region's role supplying a large portion of the world's energy needs is likely to continue in the future through a combination of hydrocarbons and alternative energy solutions. Masdar, which is based in the UAE, is one of the world's largest renewable energy and green hydrogen companies. It operates in more than 40 countries across six continents and has invested, or committed to invest, in worldwide projects with a combined value of more than US$30 billion.67

Masdar's ambitions are impressive; one of its goals is to achieve 100 gigawatts of renewable energy capacity and produce one million tonnes of green hydrogen per year by 2030, which would save more than six million tonnes in carbon dioxide emissions. In early 2023, Masdar began collaborations with four Dutch companies to develop a supply chain to transport green hydrogen from Abu Dhabi to Amsterdam, where the renewable energy will used in "key European sectors, such as sustainable aviation fuel, steelmaking, and bunkering for shipping.68, 69

Masdar aspires to become a dominant global provider in the hydrogen industry. The size of the hydrogen industry was $129 billion in 2017. Fitch Solutions predicted the industry would reach $183 billion by year-end 2023.70 The use of hydrogen as a renewable energy source is important in achieving net-zero carbon emissions by 2050, according to the International Energy Agency (IEA).71 In May 2023, the IEA released a report calling for a 60% cut in oil and gas emissions by 2030 to stay on track for the net-zero goal by 2050. The IEA estimated it would cost $600 billion to cut oil and gas emissions by almost two-thirds by 2030.72

In addition to their hydrocarbon reserves, the GCC region is still discovering vast energy deposits. In November 2023, Saudi Aramco announced that two natural gas fields had been found in the Empty Quarter Region.73 In May 2022, Abu Dhabi National Oil Company (ADNOC) announced the discovery of approximately 650 million barrels of onshore crude oil reserves.74 In April of 2018, Bahrain discovered reserves that had an estimated 80 billion barrels of oil – the largest finding since 1932.75, 76

The Price of Oil and the Sukuk Market — Understanding the Relationship

Often, there are questions and misconceptions about the risk and return relationships of sukuk originating from hydrocarbon-dependent economies. While the performance of sukuk issued by hydrocarbon-dependent economies does not have a strong relationship to hydrocarbon commodity prices, performance is not entirely insulated from oil price movements. However, there are several characteristics of sukuk that can help insulate investors from short-term oil price shocks. These include the type of sukuk structure, the behavior of sukuk relative to other asset classes, the issuer's underlying credit quality, and the sukuk's industry exposures. Over the intermediate-term to the longer-term period, the price of oil can adversely affect an issuer's credit profile, particularly with those issues directly tied to the Energy sector.

The Importance of Structure

To be considered halal, sukuk must conform to Islamic investing principles. The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) specifies that the investment certificate itself must represent "undivided shares in ownership of tangible assets, usufruct and services or (in the ownership of) the assets of [a] particular project or special investment activity."77 This requires the certificate's structure to reflect a legal transfer of ownership of the underlying assets from the issuer to the investor, or in some cases a beneficial ownership is transferred.78 Payments to the certificate holders are based on the profits of the underlying assets. The issuer cannot guarantee the security's investment return, such as a coupon rate (often referred to as the Islamic-compliant profit rate) or establish a predetermined price or principal value at the end of the investment certificate's tenure, the mark of a true risk-return relationship. This relationship is an extremely important tenet of Islamic finance that cannot be understated.

The core concepts of Islamic financial principles are to promote trade, commerce, fairness, and social justice.79 Islamic finance "merges the ethical teachings of Islam with finance as a means to meet the needs of society and to encourage socioeconomic justice."80 The term halal denotes practices, behaviors, and actions that are made in accordance with Islamic principles. If such practices, behaviors, and actions are not halal, then they are deemed haram – not being in congruence with Islamic principles.

Islamic finance uses both a principles-based framework and an exclusionary process in investing. Islamic principles promote the concept of risk-sharing. Investors share in both the potential for profits and for losses. Gharar, or the sale of what is not yet present, is discouraged. This applies to gambling, short-term speculation, and excessive risk-taking. Islam prohibits giving or receiving interest payments, also known as riba. The respective sacred texts of the three Abrahamic religions (Judaism, Christianity, and Islam) all prohibited usury, or lending with interest, because it fostered economic inequality and social injustice.81

Within Islamic finance, debt-related instruments are deemed haram due to their interest payments, lack of risk-sharing attributes, and that they are usually structured to guarantee fiscal performance regardless of the issuer's circumstances. Debt obligations are viewed in Islamic finance as risk-transferring instruments rather than risk-sharing instruments. Bond-like instruments in Islamic finance do exist, but they have been structurally modified to incorporate risk-sharing attributes. These instruments are sukuk or murabaha; the underlying instruments are tethered to the performance of the underlying assets, rather than a debt obligation. Payments of income from sukuk and murabaha are profit-sharing distributions, not interest payments.

Equities generally do not offer performance guarantees based on future results. They expose the investor and issuer to both profits and losses depending on the future performance of the underlying asset. Equity investments naturally incorporate the risk-sharing principles of Islamic finance between the issuer and the investor.

Islamic investment certificates are tethered to an underlying asset(s), and the expectation of steady income can help reduce short-term price volatility relative to energy commodities and other asset classes, such as the broader equity and bond markets. Some Islamic scholars are comfortable with a face value threshold of at least 33% physical assets underlying sukuk structures while other scholars require a threshold between 51% and 70%.82

Islamic-compliant investment certificates typically have a significant asset component within their investment structure. The assets could be tangible, such as equipment, real estate, infrastructure, or other operating assets. Some certificates are structured to have a broader range of assets and may have less tangible features. For example, Axiata, a Malaysian telecom operator, offers a certificate with income derived from cell phone usage through vouchers.83

An Islamic-compliant investment certificate may incorporate a broad range of assets only if it represents an "undivided share in the ownership," according to AAOIFI. This ownership can be direct (asset-backed sukuk) or a beneficial interest (asset-based sukuk).84 There are 14 different types of sukuk structures. Over the years the market has largely coalesced around the adoption of two types, sukuk al wakalah and sukuk al ijarah. From 2010 to 2020, 52% of total international sukuk issuance was sukuk al wakalah and 22% was sukuk al ijarah.85

Beginning on January 1, 2021, AAOIFI mandated a minimum tangible-asset ratio be maintained by all Islamic-compliant investment certificates both at the time of issuance and until the certificates' maturity. The intention was to address Shariah compliance issues, given that securities were sometimes described as "asset-light." Standard 59, also known as the "tangibility requirement ratio," mandates that the certificate's tangibility ratio must be greater than 50% at the time of issuance and must be upheld all the way through the security's issuance and maturity. Should the security's tangibility ratio drop below 51%, the issuer is required to make good on the shortfall by raising the ratio back to at least 51% within a prescribed period of time. If the tangibility ratio falls below 33% and the issuer is unable to raise it to 51% within the prescribed period, the security must be delisted.86

Furthermore, it is entirely possible for sukuk investors to obtain a higher value at the end of the investment certificate's tenure if the market value of the security's underlying asset or business enterprise appreciates at a value above its issuance. Though such an event is unlikely, it does not preclude the possibility, as the rationale is based upon the Islamic tenant of risk sharing.87 In the paper "Shariah Issues in the Application of Repurchase Undertaking in Sukuk Mudarabah," the authors state "[this] can be supported by another school of thought has it that, to be acceptable to undertake the underlying asset of Sukuk at fair value, net value, market value, or price that is agreed by both parties at the time of actual purchase according to the AAOIFI Shariah standard."

It is possible for sukuk investors to obtain a higher value when the sukuk reaches maturity if the underlying asset or business enterprise's market value appreciates at a value above its issuance.

What makes sukuk halal?

| Sukuk | Conventional Bonds | |

| Underlying Asset | Proof of ownership in an asset | Debt obligation |

| Legal Structure | Holders each hold an undivided beneficial ownership in underlying assets | Issuer has a contractual obligation to pay bond holders interest and principal on certain specified dates |

| Halal considerations | The underlying assets are halal | n/a |

| Pricing | Pricing based upon value of underlying assets | Pricing based on credit rating of issue and issuer |

| Valuation | Buyers purchase assets that have value | Buyers act as creditors in implicit loan agreement |

| Investment rewards and risks | Holders receive a share of profits from the underlying assets (and accept a share of any loss incurred) | Holders receive regularly scheduled interest payment for the life of the bond, and the principal is returned at the bond's maturity date. |

Correlation Characteristics of Sukuk Relative to Other Asset Classes.

Sukuk are a separate and distinct asset class that share many attributes with conventional fixed income. Both typically offer a stated profit rate (or coupon) and maturity, and usually are rated by major credit rating agencies. Sukuk have attributes to promote liquidity and to encourage their adoption among global investors, particularly among the secular community. Learning how sukuk correlate with other asset classes allows us to understand their risk and return characteristics.

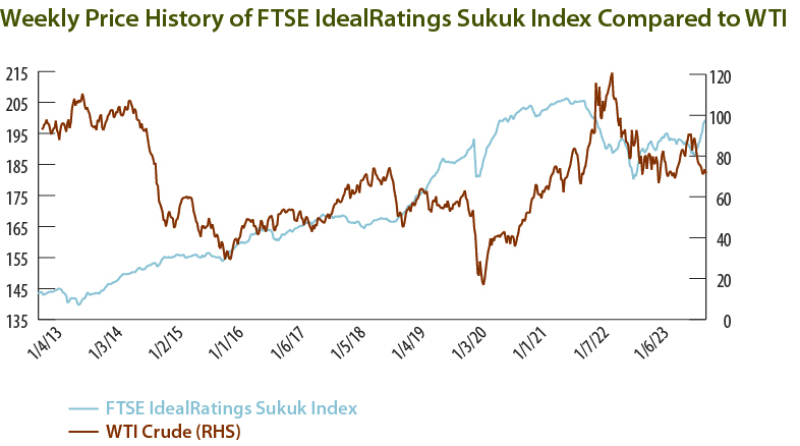

At year-end 2023, the five-year price correlation between the FTSE IdealRatings Sukuk Index and West Texas Intermediate (WTI) was 0.173. Stated differently, 17.3% of the price movement of the Index can be explained by crude oil prices, which were down from 29.3% at the prior five-year period at year-end of 2021. This five-year price correlation is notably lower than when we published the first edition of the GCC Sukuk Primer. At that point, the correlation was 36.7% for the five-year period ended March 31, 2020, reflecting a 50% reduction.

| Correlation Matrix: 5-years (December 31, 2018 - December 31, 2023) | |||||||||

| Asset Class | Crude Oil (WTI) | FTSE Sukuk | Bloomberg US Aggregate | JPMorgan EMBI Global Core | MSCI ACWI | S&P 500 | |||

| Crude Oil (WTI) | 1.000 | 0.173 | -0.007 | 0.247 | 0.299 | 0.272 | |||

| FTSE Sukuk | 0.173 | 1.000 | 0.778 | 0.804 | 0.477 | 0.439 | |||

| Bloomberg US Aggregate | -0.007 | 0.778 | 1.000 | 0.650 | 0.328 | 0.298 | |||

| JPMorgan EMBI Global Core | 0.247 | 0.804 | 0.65 | 1.000 | 0.731 | 0.666 | |||

| MSCI ACWI Index | 0.299 | 0.477 | 0.328 | 0.731 | 1.000 | 0.970 | |||

| S&P 500 | 0.272 | 0.439 | 0.298 | 0.666 | 0.970 | 1.000 | |||

| Source: Bloomberg (December 31, 2018 - December 31, 2023. Weekly Data) | |||||||||

This decline was not surprising for several reasons. First, most US dollar-denominated sukuk from the GCC are not directly tied to the Energy sector or the hydrocarbon industry. Second, many GCC sovereign issuers have prioritized the redirection of the economy away from the hydrocarbon industry. At year-end 2022, Saudi Arabia's non-oil economy, as expressed as a percentage of GDP, was 56%, with projections to rise to 71% by 2028.88 The non-oil sectors of the UAE accounted for more than 70% of the country's GDP.89 Third, the price of oil is largely managed by a consortium of oil-producing countries, such as OPEC+.90 Fourth, technical and other exogenous factors can cause extreme volatility in the price of oil. After a contentious disagreement between Saudi Arabia and Russia in April of 2020, the price of oil fell to -$40.32. The price dynamics of a commodity are not necessarily associated with the business activities of a sukuk issuer.

When comparing the FTSE IdealRatings Sukuk Index with the WTI for the three-year period ended December 31, 2023, the correlation between the two becomes more pronounced at -7.0%. When the second edition of the GCC Sukuk Primer was published, this correlation was 32.8%. Again, WTI's price decline to -$43.32 in April of 2020 can help explain the material change in correlation.

| Correlation Matrix: 3 years (December 31, 2020 - December 31, 2023) | |||||||||

| Asset Class | Crude Oil (WTI) | FTSE Sukuk | Bloomberg US Aggregate | JPMorgan EMBI Global Core | MSCI ACWI | S&P 500 | |||

| Crude Oil (WTI) | 1.000 | -0.070 | -0.096 | -0.080 | 0.164 | 0.142 | |||

| FTSE Sukuk | -0.070 | 1.000 | 0.825 | 0.755 | 0.431 | 0.387 | |||

| Bloomberg US Aggregate | -0.096 | 0.825 | 1.000 | 0.682 | 0.381 | 0.344 | |||

| JPMorgan EMBI Global Core | -0.080 | 0.755 | 0.682 | 1.000 | 0.658 | 0.573 | |||

| MSCI ACWI Index | 0.164 | 0.431 | 0.381 | 0.658 | 1.000 | 0.962 | |||

| S&P 500 | 0.142 | 0.387 | 0.344 | 0.573 | 0.962 | 1.000 | |||

| Source: Bloomberg (December 31, 2020 - December 31, 2023. Weekly Data) | |||||||||

For the three-year period ended 2023, the Bloomberg US Aggregate Total Return Index and the JPMorgan Emerging Market Bond Global Core Index exhibited strong correlations with the FTSE IdealRatings Sukuk Index. This is because all three benchmarks are entirely composed of US dollar-denominated securities.

This relationship makes sense, as sukuk are structured similarly to conventional debt. Over the past two years, correlation among these three indices experienced a slight yet negligible drift. Essentially, this means that the FTSE IdealRating Sukuk Index's performance characteristics can be explained by the movements of either benchmark.

The correlation between the FTSE IdealRatings Sukuk Index and the WTI was 17.3% for the five-year period and -7.0% for the three-year period. This large change can be attributed to the price of oil falling to -$40.32 in April of 2020. The movement of the FTSE IdealRatings Sukuk Index in correlation to the EMBI Global Core Index was less dramatic, falling from 80.4% to 75.5%. Otherwise, most of the benchmark correlations remained relatively stable over the five-year and three-year periods. The differences in correlation between the five-year and three-year periods were negligible for the period ended 2021.

| Correlation Matrix: Comparing Change in 5-year period vs. 3-year for year-end 2023 | ||||||

| Asset Class | WTI | FTSE Sukuk Benchmark | BB US Agg Total Return | JPMorgan EMBI Global Core | MSCI ACWI Index | S&P 500 |

| WTI | 0.000 | -0.243 | -0.089 | -0.327 | -0.135 | -0.130 |

| FTSE Sukuk Benchmark | -0.243 | 0.000 | 0.047 | -0.049 | -0.046 | -0.052 |

| BB US Agg Total Return | -0.089 | 0.047 | 0.000 | 0.032 | 0.053 | 0.046 |

| JPMorgan EMBI Global Core | -0.327 | -0.049 | 0.032 | 0.000 | -0.073 | -0.093 |

| MSCI ACWI Index | -0.135 | -0.046 | 0.053 | -0.073 | 0.000 | -0.008 |

| S&P 500 | -0.130 | -0.052 | 0.046 | -0.093 | -0.008 | 0.000 |

We have incorporated correlation attributes from the previous edition of this white paper for comparison.

| Correlation Matrix: 5 years (December 31, 2016 - December 31, 2021) | |||||||||

| Asset Class | WTI | FTSE Sukuk Benchmark | BB US Agg Total Return | JPMorgan EMBI Global Core | MSCI ACWI Index | S&P 500 | |||

| WTI | 1.000 | 0.293 | 0.036 | 0.399 | 0.383 | 0.350 | |||

| FTSE Sukuk Benchmark | 0.293 | 1.000 | 0.720 | 0.834 | 0.437 | 0.400 | |||

| BB US Agg Total Return | 0.036 | 0.720 | 1.000 | 0.608 | 0.156 | 0.130 | |||

| JPMorgan EMBI Global Core | 0.399 | 0.834 | 0.608 | 1.000 | 0.694 | 0.635 | |||

| MSCI ACWI Index | 0.383 | 0.437 | 0.156 | 0.694 | 1.000 | 0.962 | |||

| S&P 500 | 0.350 | 0.400 | 0.130 | 0.635 | 0.968 | 1.000 | |||

| Source: Bloomberg (December 31, 2020 - December 31, 2021. Weekly Data) | |||||||||

| Correlation Matrix: 3 years (December 31, 2018 - December 31, 2021) | |||||||||

| Asset Class | WTI | FTSE Sukuk Benchmark | BB US Agg Total Return | JPMorgan EMBI Global Core | MSCI ACWI Index | S&P 500 | |||

| WTI | 1.000 | 0.328 | 0.039 | 0.438 | 0.399 | 0.369 | |||

| FTSE Sukuk Benchmark | 0.328 | 1.000 | 0.718 | 0.847 | 0.481 | 0.452 | |||

| BB US Agg Total Return | 0.039 | 0.718 | 1.000 | 0.634 | 0.220 | 0.203 | |||

| JPMorgan EMBI Global Core | 0.438 | 0.847 | 0.634 | 1.000 | 0.748 | 0.702 | |||

| MSCI ACWI Index | 0.399 | 0.481 | 0.220 | 0.748 | 1.000 | 0.973 | |||

| S&P 500 | 0.369 | 0.452 | 0.203 | 0.702 | 0.973 | 1.000 | |||

| Source: Bloomberg (December 31, 2018 - December 31, 2021. Weekly Data) | |||||||||

| Correlation Matrix: Comparing Change in 5-year period vs. 3-year period for year-end 2021 | ||||||

| Asset Class | WTI | FTSE Sukuk Benchmark | BB US Agg Total Return | JPMorgan EMBI Global Core | MSCI ACWI Index | S&P 500 |

| WTI | 0.000 | 0.035 | 0.003 | 0.039 | 0.016 | 0.019 |

| FTSE Sukuk Benchmark | 0.035 | 0.000 | -0.002 | 0.013 | 0.044 | 0.052 |

| BB US Agg Total Return | 0.003 | -0.002 | 0.000 | 0.026 | 0.064 | 0.073 |

| JPMorgan EMBI Global Core | 0.039 | 0.013 | 0.026 | 0.000 | 0.054 | 0.067 |

| MSCI ACWI Index | 0.016 | 0.044 | 0.064 | 0.054 | 0.000 | 0.005 |

| S&P 500 | 0.019 | 0.052 | 0.073 | 0.067 | 0.005 | 0.000 |

Diversification Benefits

For investors seeking to diversify their asset allocations, sukuk may be a valuable option. The FTSE IdealRatings Sukuk Index exhibits significantly lower correlation with that of US dollar-denominated emerging market fixed-income benchmarks, while benefiting from exposure to emerging markets.

Essentially, the FTSE IdealRatings Sukuk Index exhibits lower equity correlation characteristics with the Bloomberg US Aggregate Index, yet provides investors with a more insulated exposure to emerging markets. This can create a unique balance for investors who seek diversification and emerging market fixed-income exposure, yet desire lower volatility.

A Look Back in History: Oil's Previous Price Decline and the FTSE IdealRatings Sukuk Index

The correlation matrix demonstrates that a weak relationship does exist between the price of oil and movements in the sukuk market. The price of oil does have meaningful correlation characteristics with the broad-based investment performance of sukuk. When comparing the FTSE IdealRatings Sukuk Index against the WTI, we note divergence between the two over multiple time periods.

| 10-Year | 5-Year | 3-Year | 1-Year | |||||||

| (12/31/12 - 12/29/23) | (12/31/18 - 12/29/23) | (12/31/20 - 12/29/23) | (12/30/22 - 12/29/23) | |||||||

| Total Return | Annualized | Total Return | Annualized | Total Return | Annualized | Total Return | Annualized | |||

| FTSE Sukuk Benchmark | 39.44% | 3.07% | 18.15% | 3.39% | -1.98% | -0.67% | 5.63% | |||

| West Texas Intermediate | -46.38% | -5.51% | 95.31% | 14.33% | 100.23% | 26.09% | -11.88% | |||

Past performance does not indicate any assurance of future performance. Sukuk performance and oil returns do not behave in a lockstep manner; a more complex relationship exists.

Putting a Pin in Relative Risk and Return

While the GCC sukuk market has grown rapidly in recent years, it is a nascent market subject to oil price shocks, regional tensions, fickle foreign institutional flows, and a host of other factors. Nonetheless, GCC debt and sukuk markets have demonstrated favorable risk and return profiles to warrant long-term investors' consideration. When comparing various regional and broad-based fixed-income benchmarks, the Bloomberg GCC Credit Total Index Unhedged USD and the FTSE IdealRatings Sukuk Index demonstrated competitive performance over the five-year, three-year, and one-year trailing periods ended December 29, 2023.

| 5-year Trailing Return | 3-year Trailing Return | 1-year Return | ||||||||

| (12/30/18 - 12/29/23) | (12/31/20 - 12/29/23) | (12/30/22 - 12/29/23) | ||||||||

| Total Return | Annualized | Total Return | Annualized | Annualized | ||||||

| Bloomberg GCC Credit Total Return Index Value Unhedged USD | BGCITRUU Index | 15.26% | 2.88% | -7.90% | -2.71% | 5.36% | ||||

| Bloomberg EM Asia USD Total Return Index Value Unhedged | BEUCTRUU Index | 9.01% | 1.74% | -8.48% | -2.92% | 7.07% | ||||

| Bloomberg EM Hard Currency Agg. TR Index Value Unhedged USD | LG20TRUU Index | 6.99% | 1.36% | -10.92% | -3.79% | 9.66% | ||||

| JPMorgan EMBI Global Core | JPEICORE Index | 8.79% | 1.70% | -11.41% | -3.96% | 10.84% | ||||

| FTSE Sukuk | SBKU Index | 18.15% | 3.39% | -1.98% | -0.67% | 5.63% | ||||

| Bloomberg US Treasury Index measures | LUATTRUU Index | 2.68% | 0.53% | -11.03% | -3.83% | 4.06% | ||||

| Bloomberg Global Agg Treasuries Total Return Index | LGTRTRUU Index | -7.16% | -1.48% | -19.70% | -7.07% | 4.19% | ||||

| Bloomberg US Agg Total Return | LBUSTRUU Index | 5.64% | 1.10% | -9.62% | -3.32% | 5.54% | ||||

| S&P 500 | SPX Index | 107.04% | 15.68% | 33.02% | 10.00% | 26.34% | ||||

| MSCI Emerging Markets Index | MXEF Index | 21.76% | 4.02% | -13.74% | -4.82% | 10.15% | ||||

| Crude (Oil) | CL1 Comdty | 95.31% | 14.33% | 100.23% | 26.09% | -11.88% | ||||

The FTSE IdealRatings Sukuk Index also demonstrated similar strong performance metrics relative to US fixed-income benchmarks such as the Bloomberg US Aggregate Total Return Index and the Bloomberg US Treasury Index.

We must stress that past performance does not indicate any assurance of potential future outcomes. However, the strong benchmark performance observed in this third edition of our GCC Sukuk Primer was also seen in our previous two editions. We employed the same benchmarks in each Primer edition to promote consistency and impartiality.

Risks should also be considered as an important factor to an investor. Equities can demonstrate favorable return characteristics over the long-term, yet this asset class can experience pronounced volatility in pursuit of realizing its return potential. As the adage goes, it's time in the market that is important, rather than timing the market. If one was fully invested in the S&P 500 from 1980 through 2018, save for the five highest-performing days, the investor's overall return would be reduced by 35%. In fact, missing the best 10 days between 1980 and 2018 would cut an investor's long-term results by more than 50%.98

Standard deviation measures the amount of variation, or dispersion, of a set of observed values and is commonly used to measure investment risk. In this case, the set of values comprises investment returns over time. The higher the standard deviation, the greater the dispersion of returns, both positive and negative. Greater return dispersion implies greater risk, while conversely, the lower the dispersion, the lower the risk. Standard deviation is best used in a relative framework to compare returns to other asset classes and therefore gain a sense of return variability.

Examining the five-year standard deviation among a broad range of asset class benchmarks can help position us better to estimate risk. The FTSE IdealRatings Sukuk Index demonstrated the lowest volatility when compared to the other selected benchmarks. Notably, volatility across all security indices for the five-year and three-year periods ended 2023 was lower compared to the same periods ended 2021. Volatility was also lower over the trailing three-year period ended 2023 when compared with the trailing five-year period.

| 5-year Period | 3-year Period | ||||

| 5-year Standard Deviation | Calculated Risk of Benchmark Relative to FTSE Sukuk Bnch (Expressed as a Multiple) | 3-year Standard Deviation | Calculated Risk of Benchmark Relative to FTSE Sukuk Bnch (Expressed as a Multiple) | ||

| (12/30/18 - 12/29/23) | (12/31/20 - 12/29/23) | ||||

| Bloomberg GCC Credit Total Return Index Value Unhedged USD | BGCITRUU Index | 2.3% | 1.9 | 2.0% | 1.7 |

| Bloomberg EM Asia USD Total Return Index Value Unhedged | BEUCTRUU Index | 1.8% | 1.5 | 2.0% | 1.7 |

| Bloomberg EM Hard Currency Agg. TR Index Value Unhedged USD | LG20TRUU Index | 2.5% | 2.1 | 2.4% | 2.1 |

| JPMorgan EMBI Global Core | JPEICORE Index | 3.9% | 3.3 | 3.4% | 2.9 |

| FTSE IdealRatings Sukuk | SBKU Index | 1.2% | 1.0 | 1.2% | 1.0 |

| Bloomberg US Treasury Index | LUATTRUU Index | 2.7% | 2.3 | 2.8% | 2.4 |

| Bloomberg Global Agg Treasurys Total Return Index | LGTRTRUU Index | 2.8% | 2.4 | 3.1% | 2.6 |

| Bloomberg US Agg Total Return | LBUSTRUU Index | 2.6% | 2.2 | 2.9% | 2.5 |

| S&P 500 | SPX Index | 9.7% | 8.2 | 8.0% | 6.7 |

| MSCI Emerging Markets Index | MXEF Index | 7.8% | 6.6 | 7.4% | 6.2 |

| Crude (Oil) | CL1 Comdty | 24.8% | 20.9 | 17.9% | 15.1 |

As of year-end 2023, WTI had the highest standard deviation among all the asset classes for the five-year period at 24.8%, down from 43.7% at year-end 2021. The S&P 500 Index had the second highest volatility over the same trailing five-year period at 9.7%, substantially lower than its year-end 2021 standard deviation of 18.1%. The MSCI Emerging Market Equity Index was third at 7.8%, down from 17.7%. For both the three-year and five-year periods ended 2021 and 2023, the S&P 500 demonstrated higher volatility relative to emerging market equities.

The FTSE IdealRatings Sukuk Index posted the lowest standard deviation metrics among all the benchmarks. It reported a standard deviation of 1.2% for both periods ended 2023, down from 2.9% for the five-year period and down from 3.5% for the three-year period ended 2021.

If we express the FTSE IdealRatings Sukuk Index as a single unit of risk relative to each of the other benchmarks, we can see their volatility relative to that Index. Using the five-year data for the period ended 2023 (1.2), the JPMorgan EMBI Global Core had a standard deviation of 3.9%, or 3.3x more variable than the FTSE IdealRatings Sukuk Index. The Bloomberg US Aggregate Index five-year standard deviation was 2.6%, or 2.2x more volatile. The S&P 500 Index was 8.2x more volatile, oil was 20.9x more volatile, and the Bloomberg US Treasury Index was 2.3x more volatile. The data is relatively consistent over the five-year and three-year periods.

Conclusion

On balance, GCC US dollar-denominated sukuk can be a valuable means of diversification for investors, as a distinct asset class possessing unique and favorable risk and return attributes.

The collective attributes of this region – with their large capital buffers, vast hydrocarbon reserves, and strong credit ratings – provide an appealing option for investors. The favorable investment attributes of sukuk are rarely found among emerging and frontier markets, and rarely observed among developed world fixed-income benchmarks. The steady high-decile performance metrics in conjunction with low-risk attributes warrants investors' consideration as a part of their comprehensive asset allocation.

While most investors may not have sukuk on their radar, we hope that you find this white paper useful for learning about this region, its community, and ultimately, the unique Islamic-compliant fixed-income market

Footnotes

- Wilson, Harry, and Lacqua, Francine. "Middle East Is in a Golden Era, JPMorgan's Raghaven says." BNN Bloomberg, October 2, 2023. https://www.bnnbloomberg.ca/middle-east-is-in-a-golden-era-jpmorgan-s-raghavan-says-1.1979013

- Press Release: IMF Executive Board Concludes 2023 Article IV Consultation with Saudi Arabia. International Monetary Fund, September 6, 2023. https://www.imf.org/en/News/Articles/2023/09/05/pr23302-saudi-arabia-imf-exec-board-concludes-2023-art-iv-consult

- State of the Saudi Economy Annual Report. 2022. Ministry of Economy & Planning, p. 3. https://www.mep.gov.sa/MonthlyReports/State%20of%20the%20Economy%202022%20EN.pdf

- Event Update – IMF REO – October-23. Kamco Invest, October 15, 2023. https://www.kamcoinvest.com/research/event-update-imf-reo-october-2023

- World Economic Outlook October 2023: Navigating Global Divergences. International Monetary Fund. https://www.imf.org/en/Publications/WEO/Issues/2023/10/10/world-economic-outlook-october-2023

- IMF Regional Economic Outlook: Middle East and Central Asia, October 2022, p.8. https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&cad=rja&uact=8&ved=ah UKEwiBsYmFw96DAxWUFzQIH eDkA70QFnoECBUQAQ&url= https%3A%2F%2F www.imf.org%2F%2Fmedia%2FFiles%2FPublications %2FREO%2FMCD-CCA%2F2022%2FOctober%2FEnglish%2Ftextashx &usg=AOvVaw2ujIQZM-rAb6lEjMISigrd&opi=89978449

- Nair, Deepthi. "GCC sovereign wealth funds' assets under management grow to $4 trillion." The National News, August 8, 2023. https://www.thenationalnews.com/business/economy/2023/08/09/gcc-sovereign-wealth-funds-assets-under-management-grow-to-4-trillion/

- Galloway, Lindsey. "Why is this country so resilient?" BBC News, January 6, 2022. https://www.bbc.com/travel/article/20220105-why-is-this-country-so-resilient

- Sankar, Anjana. "Ukrainian expats in Dubai long for home as war interrupts lives." The National News, February 23, 2023. https://www.thenationalnews.com/uae/2023/02/23/ukrainian-expats-in-dubai-long-for-home-as-war-interrupts-lives/

- Kane, Frank. "The hopes – and insecurities – of Russian exiles in Dubai." Arabian Gulf Business Insight, October 6, 2023. https://www.agbi.com/opinion/the-hopes-and-insecurities-of-russian-exiles-in-dubai/

- Dubai real estate: Property market hits 9-year high, breaking 2014 records." Arabian Business, November 30, 2023. https://www.arabianbusiness.com/industries/real-estate/dubai-real-estate-property-market-hits-9-year-high-breaking-2014-records

- Dubai Residential Market Outlook: Autumn 2023. 2024 Residential Forecast Edition. Knight Frank, p. 17. https://content.knightfrank.com/research/2364/documents/en/dubai-residential-market-review-autumn-2023-10737.pdf

- "Most expensive apartment in Dubai sold for Dhs410 million." Gulf Today, February 3, 2023. https://www.gulftoday.ae/news/2023/02/03/most-expensive-apartment-in-dubai-sold-for-dhs410-million

- http://dubai2040.ae/en/

- James, Edward. "GCC projects market breaks all-time spending record." MEED, November 22, 2023. https://www.meed.com/gcc-projects-market-breaks-all-time-spending-record

- State of the Saudi Economy Annual Report. 2022. Ministry of Economy & Planning, p. 20. https://www.mep.gov.sa/MonthlyReports/State%20of%20the%20Economy%202022%20EN.pdf

- Corder, John. "Saudi Arabia Says Its 100 Million Visitor Goal is 'No Longer Sufficient.'" Skift, September 27, 2023. https://skift.com/2023/09/27/saudi-arabia-visitor-target-middle-east-newsletter/

- Ritter, Jeff and Schwarb, John. "Q&A: The PGA Tour and LIV Golf Have Merged. Here's What We Know." Sports Illustrated, June 12, 2023. https://www.si.com/golf/news/pga-tour-and-liv-golf-have-merged-frequently-asked-questions

- Draper, Kevin. "The Alliance of LIV Golf and the PGA Tour: Here's What to Know." The New York Times, June 7, 2023. https://www.nytimes.com/2023/06/07/sports/golf/pga-liv-golf-merger.html

- Michaelson, Ruth. "Revealed: Saudi Arabia's $6bn spend on 'sportswashing.'" The Guardian, July 26, 2023. https://www.theguardian.com/world/2023/jul/26/revealed-saudi-arabia-6bn-spend-on-sportswashing

- "Gulf Cooperation Council." Britannica, January 27, 2024. https://www.britannica.com/topic/Gulf-Cooperation-Council

- IFM Sukuk Report, 12th edition. International Islamic Financial Market, August 2023. pp. 81. https://www.iifm.net/frontend/general-documents/f0a12d4a6880f8e3bc23a23a03baa8e61693983390.pdf

- IIFM Sukuk Report, pp. 58.

- "Gulf nations witness 178% surge in US Dollar sukuk issuance: Fitch Ratings." Arab News, January 14, 2024. https://www.arabnews.com/node/2441406/business-economy

- IIFM Sukuk Report, pp. 85.

- IIFM Sukuk Report, pp. 104.

- IIFM Sukuk Report, pp. 53.

- Saba, Yousef. "Egypt to raise $1.5 billion with debut sukuk at 11% yield." Reuters, February 21, 2023. https://www.reuters.com/markets/rates-bonds/egypt-raise-15-billion-with-debut-sukuk-11-yield-2023-02-21/

- "Philippines Debuts in the Islamic Finance Market with First US-Dollar Sukuk." BNN Breaking News, November 28, 2023. https://bnnbreaking.com/finance-nav/philippines-debuts-in-the-islamic-finance-market-with-first-us-dollar-sukuk/

- Suhartono, Harry and Karve, Ameya. "Philippines Selling Debut Islamic Bond Amid Drop in Spreads." Bloomberg News, November 28, 2023. https://www.bloomberg.com/news/articles/2023-11-29/philippines-starts-marketing-its-debut-dollar-islamic-bond

- "Bank ABC arranges landmark US$600 million Sukuk issuance for Air Lease Corporation (ALC)." PR Newswire, March 22, 2023. https://www.prnewswire.com/news-releases/bank-abc-arranges-landmark-us600-million-sukuk-issuance-for-air-lease-corporation-alc-301778777.html

- "Emirates NBD arranges Air Lease Corporation's US$600 million inaugural sukuk." Emerites News Agency-WAM, March 21, 2023. https://wam.ae/en/details/1395303141067

- Upadhyay, Rakesh. "How Realistic Is Saudi Arabia's $2 Trillion Sovereign Wealth Fund?" Oilprice.com, April 7, 2016. https://oilprice.com/Energy/Energy-General/How-Realistic-Is-Saudi-Arabias-2-Trillion-Sovereign-Wealth-Fund.html

- Kassem, Mahmoud. "Abu Dhabi raises $5bn from first bond sale in seven years." The National, April 26, 2016. https://www.thenational.ae/business/markets/abu-dhabi-raises-5bn-from-first-bond-sale-in-sevenyears-1.142390

- "Abu Dhabi says to fund wider 2016 deficit mainly via bond issues." Reuters, April 24, 2016. https://www.reuters.com/article/abu-dhabi-bonds/abu-dhabi-says-to-fund-wider-2016-deficit-mainly-via-bond-issuesidUSL5N17R0E6

- "Abu Dhabi's $5-billion bonds heavily oversubscribed." Emirates 24/7, May 10, 2016. https://www.emirates247.com/business/economy-finance/abudhabi- s-5-billion-bonds-heavily-oversubscribed-2016-05-10-1.629695

- Hamzah, Al-Zaquan Amer, and Torchia, Andrew. "Malaysia central bank sukuk pull-back opens door wider for other issuers." Reuters, July 9, 2015. https://www.reuters.com/article/idUSL8N0ZO1KE/

- Elliott, Larry. Global financial crisis: five key stages. The Guardian, August 7, 2011. https://www.theguardian.com/business/2011/aug/07/global-financial-crisis-key-stages

- "Fitch Downgrades the United States' Long-Term Ratings to 'AA+' from 'AAA'; Outlook Stable." Fitch Ratings, August 1, 2023. https://www.fitchratings.com/research/sovereigns/fitch-downgrades-united-states-long-term-ratings-to-aa-from-aaa-outlook-stable-01-08-2023

- "Fitch Affirms United Kingdom at 'AA-'; Outlook Negative." Fitch Ratings, June 2, 2023. https://www.fitchratings.com/research/sovereigns/fitch-affirms-united-kingdom-at-aa-outlook-negative-02-06-2023

- "China Credit Brief: September 2023." Fitch Ratings, September 27, 2023. https://www.fitchratings.com/research/structured-finance/china-credit-brief-september-2023-27-09-2023

- "Government Budget." Unified National Platform GOV.SA, FY 2023. https://www.my.gov.sa/wps/portal/snp/aboutksa/governmentBudget/!ut/p/z1/jZDLDoIwEEW_hi0zFVDjroKJIFobX9iNQVOrBqlBFD_fBt2Y-JrdTM65uRkQkIDI0-tepeVe52lm9qVoroahHyJzCUNv7iCnvZHrRkEDWwiLGojGbZdQJIw5Xhe5P2wxOpkTRA_EPz5-GIq__InMTYaosQGPsd81GBuRJnI-Dfx4MGuYnCfwrWYNfOkRgVCZXj9-QvO101YgCrmVhSzsS2HOu7I8nTsWWlhVla20Vpm0N_po4Ttlp88lJK8knI6z5BYevOwa0zuAzb0X/#header2_3

- "Moody's changes US ratings outlook to negative, affirms AAA." Reuters, November 10, 2023. https://www.reuters.com/markets/us/view-moodys-changes-us-ratings-outlook-negative-affirms-aaa-2023-11-10/

- Ozer, Alon. "Omnia Observations: The United States vs. Oil and the Changing Macro Fundamentals." OMNIA Family Wealth, April 2022. https://omniawealth.com/omnia-observations-the-united-states-vs-oil-and-the-changing-macro-fundamentals/

- Al-Hamidy, Abdulrahman and Banafe, Ahmed. "Foreign Exchange Intervention in Saudi Arabia." October 2013. BIS Paper No. 73v. https://ssrn.com/abstract=2474007

- Marzovilla, Olga and Mele, Marco. "From dollar peg to basket peg: the experience of Kuwait in view of the GCC monetary unification." March 2010. MPRA Paper 21605, p. 5. https://mpra.ub.uni-muenchen.de/22484/3/From_Dollar_Peg_to_basket_peg_the_experience_of_kuwait.pdf

- "Utd. Arab Emir. Dirham Currency. – AED." OANDA FX Data Services. https://www.oanda.com/currency-converter/en/currencies/majors/aed/

- Marzovilla, Olga and Mele, Marco. "From dollar peg to basket peg: the experience of Kuwait in view of the GCC monetary unification." March 2010. MPRA Paper 21605. https://mpra.ub.uni-muenchen.de/22484/3/From_Dollar_Peg_to_basket_peg_the_experience_of_kuwait.pdf

- "About Us – Our history." Aramco. https://www.aramco.com/en/who-we-are/overview/our-history

- "Top 100 Largest Fund Rankings by Total Assets." Sovereign Wealth Fund Institute. https://www.swfinstitute.org/fund-rankings/sovereign-wealth-fund

- Al Flaiti, Ali. "Demographics Of The GCC – Understanding The Changes In The Local Population." International Statistical Institute, July 19, 2023. https://www.isi2023.org/abstracts/submission/746/view/

- "Expat numbers fell sharply in 2020-21." PwC, May 2023. https://www.pwc.com/m1/en/publications/middle-east-economy-watch/population-trends.html

- Al Flaiti, Ali. "The Role of the Expatriate Population (Non-GCC Citizens) in the Overall Population Growth and Structure." International Statistical Institute, July 17, 2023, p. 3. https://www.isi2023.org/media/abstracts/ottawa-2023_ff141f9ec5e43302df5b35a5b55139b8.pdf

- Kuwait Investment Authority. https://kia.gov.kw/investments