The Slowest Moving Train Wreck in History Picks Up Speed

Key Takeaways

- Social Security’s finances are on an accelerating decline. Without policy changes, the retirement trust fund is projected to be depleted around 2032, which could trigger across the board benefit cuts rather than full payments for many retirees.

- The core problem is structural, not temporary. A shrinking ratio of workers to retirees, past policy choices (like lower taxation of benefits and income caps), and demographic trends mean that even if Congress patches the 2032 shortfall, similar funding gaps are likely to reappear.

- Individuals cannot rely on Social Security and Medicare alone. Building additional retirement savings—starting early, saving consistently, and considering tools like tax advantaged accounts and HSAs where appropriate—remains critical to maintaining financial security and covering future healthcare costs.

Just over 12 years ago, in March 2014, Saturna’s Founder Nicholas Kaiser published one of our first “From the Yardarm” newsletter articles titled Recalibrating the Retirement Clock: Should 75 be the new 65? In that article, Nick observed most Americans’ savings were insufficient to cover their retirement expenses and there were substantial risks associated with relying on Social Security, which was never designed to be a national pension plan. Foremost among those risks was, “Social Security trustees anticipate that by 2033 tax revenues will only be sufficient to cover three-quarters of ‘scheduled benefits.’” Since the article’s appearance, what steps has the government taken to address the looming shortfall?

They have exacerbated the problem by reducing taxes on Social Security payments in the One Big Beautiful Bill Act, through immigration policy and with the bi-partisan Social Security Fairness Act, which extended payments to some public sector workers whose benefits were previously limited. As a result, the 2033 date has now been brought forward to 2032. Nick, being a prescient thinker, anticipated such risks and advised investors to save early, often, and as much as possible. With only six years remaining until 2032, we thought it made sense to check in on the current state of the Social Security Administration (SSA), this also included examining Medicare.

A Social Security Refresher

Roughly 76% of Social Security benefits are paid to retirees, while spouses, survivors, and disabled workers receive the remainder. Benefits are funded primarily by payroll contributions, with workers and employers each paying a 6.2% tax that together provides about 91% of total funding. Additional funding comes from interest earned and taxes paid on Social Security benefits.1 Payroll earnings are subject to Social Security tax only up to a wage cap that rises each year and is set at $184,500 for 2026. While an impressive salary, we immediately notice that Social Security taxes are regressive. Anyone earning up to the income cap will pay 6.2%, while the percentage declines for every additional dollar earned above that level. If your salary is $369,000 your Social Security tax rate drops to 3.1%. Of course, earnings above the income limit do not entitle you to additional Social Security benefits, which are also capped. In 2026 the maximum monthly payout for someone retiring at age 70 stands at $5,181.2

Benefits are primarily funded by payroll contributions, and the structure of that funding warrants a closer look. In earlier decades, Social Security payroll tax revenues exceeded benefits paid. The surplus taxes collected were invested in US Treasuries and held in one of two Social Security trust funds. Starting in 2010, however, benefit payments outstripped taxes collected, and the Social Security administration was forced to start tapping the trust funds. Last year, the Social Security Board of Trustees forecasted the retirement trust fund would be depleted in 2033, requiring benefit cuts in 2034. That was one year earlier than they had projected in 2024. The Trustees’ latest report projects that the retirement trust fund will be depleted in 2032. We’re detecting a pattern. By law, the SSA cannot run a deficit, so total benefits will be constrained by incoming tax revenue, and in late 2032 the average recipient could see benefit cuts of 22%.3 Trustees cited declining fertility rates, reduced tax collection on Social Security payments, and reduced immigration cutting the number of workers paying into the system for their revised projections.

Have We Been Here Before?

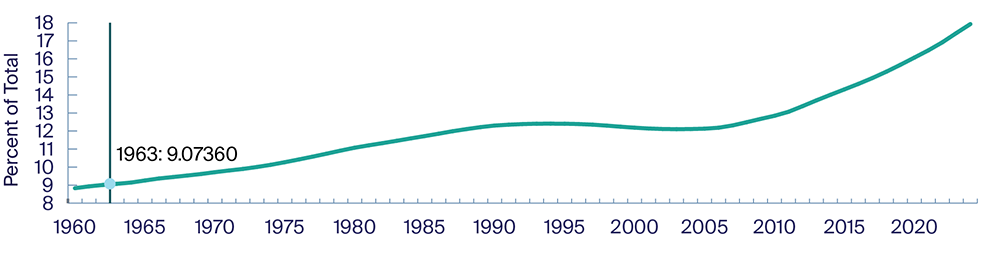

Yes! Politically speaking, six years seems like a short runway, however in 1983 the SSA was a mere three months from being unable to pay full benefits until bi-partisan Social Security reform was signed into law by President Reagan. Several features of that legislation are worth reviewing. First and probably most important, existing beneficiaries were hardly affected, which we can likely explain by noting 75% voter participation among those 65 and above versus 48% for those aged 18 to 24.4 Those numbers will loom even larger come the 2030’s as the last of the baby boomers will have aged into senior citizenship. In 1983 only 11.5% of the population was aged 65 and above, while by 2031 over 20% will be in that age cohort,5 nearly doubling their voting power.

A fairness concern was also at play, since retirees have few practical options to supplement their income. To meet the funding challenge the 1983 reform briefly suspended cost-of-living increases, raised the retirement age, accelerated previously scheduled increases of payroll income caps and raised the Social Security tax from 5.4% each for employee and employer to 5.7% each in 1984, 6.06% each in 1989, and to the current 6.2% in 1990. Taxes were also levied on Social Security benefits for the first time.

Population ages 65 and above for the United States

Source: World Bank via FRED®

Are We Likely to See a Similar Resolution?

Cautiously optimistically, yes. While Democrats and Republicans stand far apart on most issues, there’s strong bi-partisan interest in re-election and it’s challenging to think of an issue more damaging to that quest than cutting benefits for seniors. One of the most proposed solutions is to raise the retirement age, an idea that tends to be most popular among higher-income, white-collar workers. While it is true that life expectancy has been increasing,6 there is a correlation between income levels and life span. Raising the retirement age disadvantages those who need the money the most and, due to occupation, are forced to stop working earlier than a typical desk jockey. We’re not just speaking of construction workers either. Dental hygienists often stop practicing or sharply reduce hours in their 40’s and 50’s due to repetitive stress. Nurses are similar. Many occupations are difficult to pursue into one’s 70’s, which is how long one must wait to maximize benefits.

We anticipate the government will revisit the 1983 playbook by raising the tax rate and the top level of income subject to Social Security taxes. Interestingly, while Social Security’s top taxable income level has remained roughly similar over the years in terms of percentile ranking of US incomes, earnings above the cap have exploded with rising income inequality. When Social Security launched in 1937 around 97% of total wages paid were subject to the tax. That has declined to roughly 83% today. There may be a temptation to alter the cost-of-living adjustments, while means testing for benefit payments will likely come into play. We believe both would encounter significant senior voter and political opposition. We also anticipate a return to 1983’s drama in terms of Congress delaying until the last possible minute.

So, We’re Good?

Not so fast. Even if current Social Security shortfalls are sorted, the core challenge will remain for decades — a declining ratio of workers to retirees. From 1975 through 2008 the ratio consistently ranged from 3.2 to 3.4. By 2020, the figure had slipped to 2.9 and by 2075, is forecast to drop to 2.7 Absent any changes to the government’s anti-immigration position, or higher fertility rates, the real figure will likely be lower. Whatever steps are taken to address the 2032 shortfall, a meaningful fix will require more than incremental adjustments. Given the worsening worker-to-retiree ratio, the problem is likely to resurface, and sooner than the five decades since the last major reform. For those yet to retire, the risk remains significant. Therefore, we reiterate our Founder’s wise advice to save and invest early, often, and as much as possible.

Wait, There’s More

While we’re on the topic, readers may also wonder about the outlook for Medicare, which is likewise financed through payroll and employer taxes. The tax rate stands at a lower 1.45% but there is no salary cap – every dollar earned pays the tax. Like Social Security, Medicare has two trust funds, and the Trustees of those funds also provided an update where they anticipate the funds being depleted, coincidentally, by 2033, after which Medicare would be able to pay only 89% of scheduled benefits. Medicare was included in the previously discussed 1983 Social Security legislation, but the reforms enacted were considerably more complex than for Social Security and are beyond the scope of this paper.

From an individual’s perspective the solution to the Medicare conundrum lies not only in sufficient saving but also in choosing the appropriate savings vehicle. For many, if not most, one approach stands head and shoulders above the rest — Health Savings Accounts (HSA). HSAs allow the saver to make pre-tax contributions, invest the contributions and have them grow tax-deferred, like a 401(k) or Individual Retirement Account (IRA), and here’s the kicker — allow the investor to withdraw the funds tax-free for qualified medical expenses. It behaves like a 401(k) or IRA during the contribution and tax-deferred investment phases, and morphs into a Roth IRA during the withdrawal phase, a tax trifecta unlike any other.

The current annual contribution limit stands at $4,400 for individuals and $8,750 for families with a $1,000 catch up for those 55 and older. Making those contributions over a few decades and considering potential investment returns could potentially lead to a healthy nest egg by the time retirement arrives.

There are important caveats, the most significant being that using an HSA requires enrolment in a high-deductible health plan. The minimum annual deductible for individual coverage must be at least $1,700 this year and $3,400 for families, and the maximum out-of-pocket limit is set at $8,500 for individuals and $17,000 for families. For people with substantial ongoing medical costs, the benefits of an HSA can be much less pronounced.

Finally, if you are already fully funding an IRA or 401(k), but cannot comfortably afford additional pre-tax HSA contributions, this strategy may not be practical. However, if those constraints don’t apply, an HSA’s triple tax advantage can make it an effective tool for preparing to meet future healthcare costs in retirement.