Renewable Energy: Climate Change and the Global Electric System

This is Part One of a three-part series about the transition to a low-carbon economy by way of electrification, one of the most important strategies for reducing global carbon emissions. Part One includes:

- The role renewable energy generation technologies, such as wind and solar, will play in the transition.

- The future of renewables markets compared to natural gas and coal.

- How increasing investment in the global electric system benefits the environment and helps achieve the goals of the Paris Agreement.

- The supply and demand of oil as the electric vehicle (EV) market grows.

- How different governments are using policies and subsidies to spur investment in renewable energy.

In 2015, world leaders attending the United Nations Climate Change Conference signed the Paris Agreement to address climate change and its potential risks. One of the long-term goals set by this international treaty was to limit global temperatures from rising more than 1.5°C above pre-industrial levels for the remainder of the 21st century. However, at the current rate of greenhouse gas (GHG) emissions, global temperatures are expected to rise 3-4°C by the year 2100. Global warming increases the occurrence and intensity of extreme weather such as heatwaves, floods, and hurricanes. Collapsing food security combined with soaring costs would cause massive human suffering and economic losses.1 Events of this magnitude could have dramatic, disruptive, and potentially violent geopolitical ramifications.

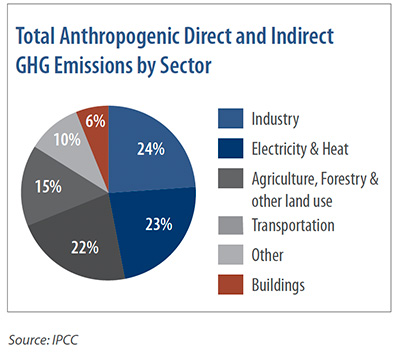

But we are not there yet. While there are numerous sources of GHG emissions, this multi-part series will focus on the challenges and opportunities in adopting renewable energy and shifting away from fossil fuels. When combined with the electrification of transportation and heating, renewables can cost-effectively address nearly 40% of GHG emissions.2

Another goal of the Paris Agreement is to achieve net-zero emissions by 2050, striking a balance between the total GHG emissions released into the atmosphere against the total emissions being removed. To reach this goal, annual investments in the global electric system (which includes generation and distribution assets) will need to reach $2.2 trillion by 2030, up from $760 million spent in 2019. We note that while this is a large increase in investment, it is still less than the individual market caps of Apple and Microsoft. The International Energy Agency (IEA), in their annual World Energy Outlook report from 2020, said that expanding and modernizing distribution networks will cost roughly one-third of the estimate, with the rest spent on generation assets.3 It will take more than just replacing coal furnaces with windmills to lower GHG emissions or limit global temperature rises. The transition requires updates to the electric grid to cope with distributed energy generation, batteries to provide dispatchable energy, and heat pumps to electrify heating.

Integrating renewables into the grid will require working with distinct yet interrelated industries in renewable energy generation, utilities, batteries, and grid infrastructure, as well as the raw materials and minerals used for each of these industries. We will explore the trends, opportunities, and roles of each industry in mitigating climate change in three sections, starting with renewable energy generation technologies.

The Role of Renewables

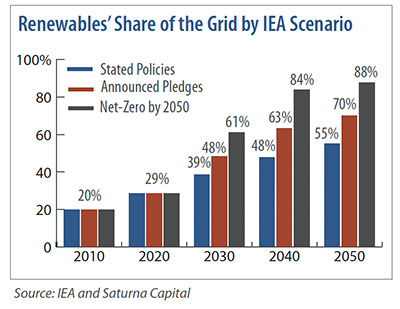

Fossil fuels account for approximately 80% of global energy consumption, including 61% of electricity generation.4,5 Disruption is coming. Over the next decade, renewable energy will capture at least 80% of the growth in electricity, increasing the share of renewables from 29% in 2020 to 39%-61% in 2030. For the same 10-year period, coal’s contribution to global energy consumption is expected to fall from 35% to 28%, and natural gas from 23% to 22%.6

Solar power is expected to be the greatest beneficiary over the coming decades. In the IEA’s 2020 report, executive director Faith Birol said, “I see solar becoming the new king of the world’s electricity markets.” In its ascension to the throne, solar generation’s compound annual growth rate (CAGR) is predicted to range from 20% to 26% on an annual basis between 2022 and 2030, capturing anywhere from 61% to 75% of growth.7 Meanwhile, wind power is expected to grow 12% to 16% on an annual basis over the same period.8

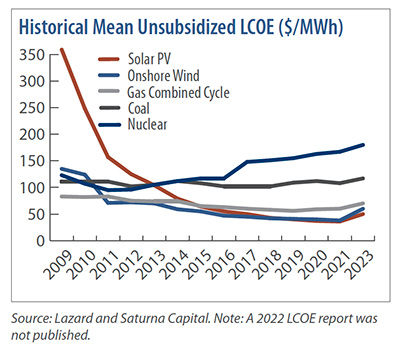

Why is solar expected to outgrow wind? Many point to the rapidly falling costs of solar panel production, which has helped lower the levelized cost of energy (LCOE) until it was cheaper than wind energy. However, the consistency of solar energy (while an enabler) makes a greater contribution than wind and does not feature in LCOE calculations.

Effective load carrying capacity (ELCC) measures how much power can get to the grid when it is needed most. Wind has an ELCC of 62% when combined with batteries holding four hours of energy storage (to offset the intermittency of wind and solar). In other words, a 100-megawatt wind farm can reliably provide 62 megawatts of power. Solar, on the other hand, has a 99% ELCC.9 A wind farm would need 1.6x the capacity of a solar array to provide the same amount of reliable energy. To be sure, there are wind utilization opportunities. Some places, like the English coast and the prairies of Canada, are naturally dark and windy. After the sun sets, the wind can still blow. Still, en masse, the economics of solar are better.

The economics of renewables are attractive, despite mixed media attention. While higher interest rates raise the cost of capital for deploying new renewable developments, fossil fuels are subject to similar increases. In the IEA’s 2023 World Energy Outlook report, forecasts for renewable deployment increased and forecasts for natural gas modestly decreased, signaling that interest rates are energy-source agnostic.

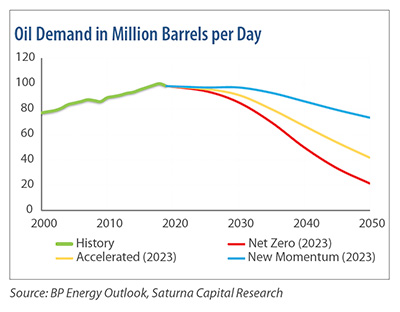

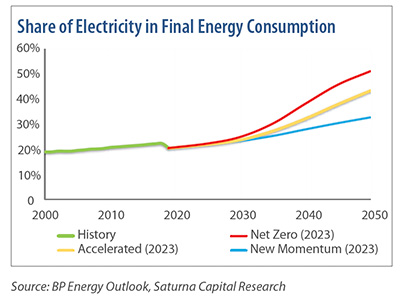

As the grid transitions to renewables, it must also expand to power transportation. Previous forecasts of when global oil consumption would peak were supply-based and failed to appreciate that rising energy prices drive innovation (e.g., fracking). Recent calls for peak oil consumption have become based on demand, and these calls weren’t limited to environmental groups, either. BP recently acknowledged that the world may have already passed peak oil consumption, while Shell expects a peak to occur in the late 2020s or early 2030s.10 To achieve the goals stated in the Paris Agreement, electricity’s role in energizing the economy will need to grow from roughly 20% in 2019 to over 50% by 2050.11

Governments around the world have enacted policies and offered subsidies to spur investment in renewables. As of year-end 2022, 128 countries had economy-wide targets for renewable energy with 31 countries calling for 100% renewable energy, mostly by 2050.12 Among the largest incentives regimes are the US Inflation Reduction Act (IRA), the European Union’s REPowerEu and Fit for 55, and China’s 14th Five-Year Plan (FYP) on renewables.

The IRA was signed into law in August 2022. Within a year, $15.9 billion was directed toward private investments in the solar and wind sectors.13 In Europe, the REPowerEU plan allocates €300 billion in grants and loans to help the trade bloc reach its target of 45% renewable energy by 2030.14 In June of 2022, China released the renewable portion of its 14th FYP, which called for doubling renewables generation from year-end 2020 to year-end 2025.15 This builds on China's target to reach 1,200 gigawatts (GW) of renewable capacity by 2030, enough to power more than 200 million US homes. To date, China looks set to blow past this target, having invested more than $39 billion in solar in 2022 (+233% from 2021), with analysts estimating the country could reach 1,000 GW of solar by 2026.16,17

As renewables become a major source of energy, their ascent will not be smooth. Government interests can create perverse incentives and supply chain challenges. Economic slowdowns and the development of critical minerals may temporarily derail the electrification of global economies. A rapid increase in renewable deployment may seem volatile in the moment, if recent media attention and investor disdain for the sector are any indication. Regardless, the technologies are available, cost-effective, and (as 2023 was officially declared the hottest year on record) desperately required.18