GCC Sukuk: A Primer, 3rd Edition Summary

Most people are not familiar with the term sukuk, much less know of their similarities to conventional fixed-income bonds. Sukuk have coupon rates and stated maturities, and they are typically rated by major credit rating agencies. The sukuk market is anticipated to reach $1 trillion in the anticipated near-term future.1 Investors that allocate a portion of their investments in global bonds are likely to already hold sukuk, as they are widely held by fund managers and mainstream exchange traded funds (ETFs) such as JPMorgan Emerging Markets Bond Index.

What Are Sukuk

Sukuk are financial certificates that adhere to Islamic law. They perform similarly to traditional bonds but have a different construction and mode of producing returns. Unlike debt instruments, sukuk represent an ownership interest in an underlying asset. The underlying assets can be tangible or intangible and must avoid activities prohibited by Islamic principles, such as charging or receiving interest (riba). Returns are generated through profit-sharing arrangements based upon the assets linked to the security. Sukuk are subject to a fatwa, a non-binding religious review, by Islamic scholars who ascertain the instrument’s adherence to Islamic law. These qualities set sukuk apart from conventional debt-based instruments.

History & Size

Records of Islamic-compliant finance date back to 700 CE.2 However, the use of sukuk in capital markets is relatively recent. The first sukuk was issued in 1990 by Shell MDS Sdn Bhd (the Malaysian subsidiary of the former energy company Shell Corporation) for 125 million Malaysian ringgit.3 Since then, the sukuk market has expanded in size and depth. At year-end 2023, the total volume of outstanding global sukuk was over $850 billion, even larger than the high yield eurodollar bond market, estimated at over $750 billion.4 Sukuk have been issued in 27 different currencies. The largest share of the sukuk market is denominated in Malaysian ringgit, followed by the US dollar.5 As of 2022, approximately 18% of the $4.5 trillion in assets that adhere to Islamic principles are represented in the global sukuk market.6 Comparing the global Muslim population—which surpassed 2.0 billion in 2023 – to the quantity of assets that adhere to Islamic principles, Islamic-compliant financial assets are notably underrepresented.7

What’s the Appeal

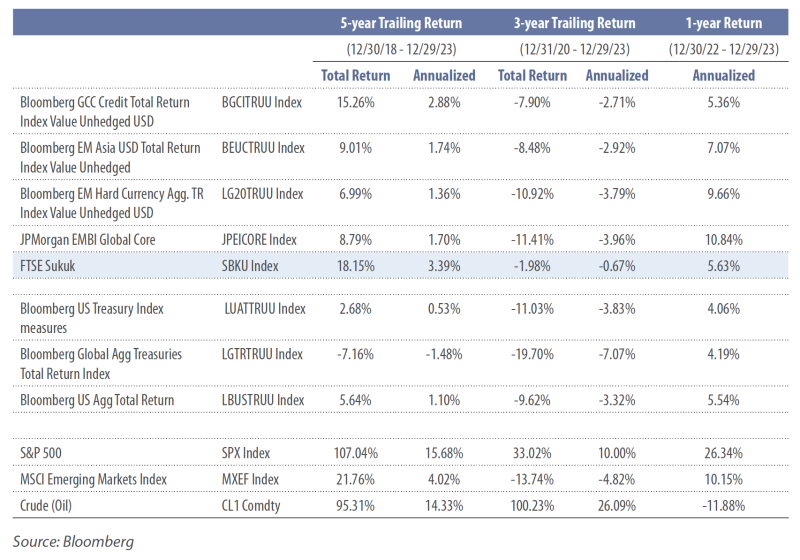

US dollar-denominated sukuk demonstrate some of the highest risk-adjusted returns among developed and emerging market fixed-income benchmarks. This portion of the market is heavily represented by sukuk issued in one of the six countries of the Gulf Cooperation Council (GCC.) We often refer to this portion of the sukuk market with the tag line “plenty in the bank, plenty in the tank,” in reference to the region’s large capital and hydrocarbon reserves.

The GCC is a political and economic alliance that was established in 1981 to promote stability and security. The council includes Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE). As of 2022, over 56 million people live in the GCC region, representing 0.7% of the global population. While the region generates just 2.2% of global gross domestic product (GDP), it satiates 32.8% the world’s oil demand, which gives the GCC significant influence on the world stage. However, about half of the population of the GCC are expatriates. This reduces the GCC’s “natural population” to about 27.6 million people.8,9 In no other region of the world is there so much wealth concentrated among such a small population. The combination of these factors (large capital buffers, extensive hydrocarbon reserves, and sukuk structuring) partially explains the favorable investment attributes of this emerging asset class.

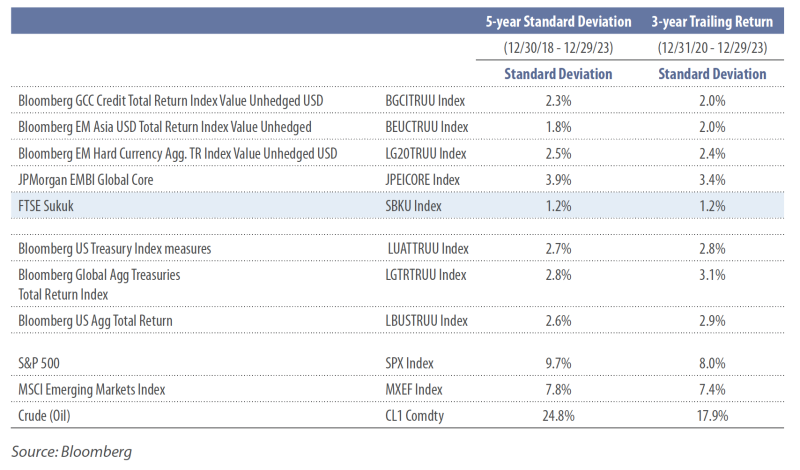

While returns are an important part of an investor’s equation, risk should also be considered. Standard deviation measures the amount of variation, or dispersion, of a set of observed values and is commonly used to measure investment risk. In this case, the set of values comprises investment returns over time. The higher the standard deviation, the greater the dispersion of returns — both positive and negative. Greater return dispersion implies greater risk, while lower dispersion signals lower risk. Standard deviation is best used in a relative framework to compare returns to other asset classes and gain a sense of return variability. We examined the five-year and three-year standard deviations among a broad range of benchmarks to help us better estimate risk. The FTSE IdealRatings Sukuk Index demonstrated the lowest volatility when compared to the other selected benchmarks.

Conclusion

On balance, US dollar-denominated sukuk issued in the GCC region can provide investors a valuable means of diversification with a distinct asset class that possesses favorable risk and return characteristics. The large capital buffers, vast hydrocarbon reserves, and strong credit ratings are appealing attributes for investors. We invite you to read our white paper, the GCC Sukuk Primer, 3rd Edition, for a more detailed look into this region, its community, and the unique Islamic-compliant fixedincome market.

Footnotes

1 “Gulf nations witness 178% surge in US Dollar sukuk issuance: Fitch Ratings.” Arab News, January 14, 2024. https://www.arabnews.com/node/2441406/business-economy

2 Alrifai, Tariq. “Islamic Finance and the New Financial System.” Wiley Finance Series, 2015. Page 11. http://candrafajriananda.lecture.ub.ac.id/files/2017/09/Wiley-finance-series-Alrifai-Tariq-Islamic-finance-and-the-newfinancial-system-_-an-ethical-approach-to-preventing-future-financial crises-Wiley-2015.pdf

3 The Sukuk Handbook: A Guide to Structuring Sukuk. Latham & Watkins LLP. Page 2. https://www.islamicfinance.com/wp-content/uploads/2015/06/Guide-to-structurings-sukuk-2015.pdf

4 Ibid. Arab News.

5 https://www.iifm.net/frontend/general-documents/f0a12d4a6880f8e3bc23a23a03baa8e61693983390.pdf (page 85)

6 ‘ICD-LSEG Islamic Development Report 2023, Navigating Uncertainty.’ https://api.zawya.atexcloud.io/file-delivery-service/version/c:NWI4OWQ5MjctNWQ3NS00:NWM3MjBmN2ItYjNjMS00/IFDI%202023%20Report%20-%20Nov%2030.pdf

7 Zouitan, Sara. “Global Muslim Population Exceeds 2 Billion. Morocco World News, April 6, 2023. https://www.moroccoworldnews.com/2023/04/354870/global-muslim-population-exceeds-2-billion

8 “Population trends: Expat numbers fell sharply in 2020-21.” PwC Middle East. https://www.pwc.com/m1/en/publications/middle-east-economy-watch/population-trends.html

9 Al Flaiti, Ali Sulaiman. “The Role of the Expatriate Population (Non-GCC Citizens) in the Overall Population Growth and Structure.” ISI World Statistics Congress, July 17, 2023. Page 3. https://www.isi2023.org/media/abstracts/ottawa-2023_ff141f9ec5e43302df5b35a5b55139b8.pdf

Important Disclaimers and Disclosures

This material is for general information only and is not a research report or commentary on any investment products offered by Saturna Capital. This material should not be construed as an offer to sell, or the solicitation of an offer to buy, any security in any jurisdiction where such an offer or solicitation would be illegal. To the extent that it includes references to securities, those references do not constitute a recommendation to buy, sell, or hold such security, and the information may not be current. Accounts managed by Saturna Capital may or may not hold the securities discussed in this material.

We do not provide tax, accounting, or legal advice to our clients, and all investors are advised to consult with their tax, accounting, or legal advisers regarding any potential investment. Investors should not assume that investments in the securities and/or sectors described were or will be profitable. This document is prepared based on information Saturna Capital deems reliable; however, Saturna Capital does not warrant the accuracy or completeness of the information. Investors should consult with a financial adviser prior to making an investment decision. The views and information discussed in this commentary are at a specific point in time, are subject to change, and may not reflect the views of the firm as a whole.

All material presented in this publication, unless specifically indicated otherwise, is under copyright to Saturna. No part of this publication may be altered in any way, copied, or distributed without the prior express written permission of Saturna.