Behind the Scenes: A Closer Look at the Amana Participation Fund Investment Process, 2nd Edition

In this informational article, we answer some commonly asked questions about the Amana Participation Fund's investment process.

We address the following questions:

- What is the Islamic compliance process around sukuk?

- Why is there performance disparity between the Amana Participation Fund and the FTSE IdealRatings Sukuk Index?

- What does it mean if an issuer is not rated by credit rating agencies? How prevalent is this rating among sukuk issuers?

- Can the Fund invest in sukuk that is not denominated in the US dollar? What is your philosophy on investing in these securities?

- Why does the Fund have a large geographic exposure to Middle Eastern issuers? How large is the sukuk market?

- What are the most common types of sukuk? Does the type of sukuk structure affect its credit rating?

- In what ways are sukuk similar to municipal appropriation bonds?

- What is your investment process?

- What criteria would cause you to sell sukuk?

- How does your team mitigate risk?

1. What is the Islamic compliance process around sukuk?

The Amana Participation Fund's primary investment objectives are capital preservation and current income, consistent with Islamic principles. Issuers of Islamic investment certificates, or sukuk, publish a prospectus for each security. We examine each issuer's prospectus to ascertain the security's Islamic compliance. If the security is Islamic-compliant, we then examine the investment's merits for potential inclusion in the portfolio. If there is no affirming language of the security's Islamic compliance, we do not proceed.

Here are three examples of the language that issuers use to note their Islamic compliance.

Saudi Arabian food company Almarai issued sukuk in 2019. Their offering document states:

Each of the Shariah Supervisory Board of First Abu Dhabi Bank PJSC, the Executive Shariah Committee of HSBC Saudi Arabia, the Shariah Supervisory Committee of Standard Chartered Bank and the Global Shariah Supervisory Board of Gulf International Bank has confirmed that the Transaction Documents are, in their view, Shari'a compliant.1

The emirate of Dubai issued a 10-year sukuk in September of 2020. Page 11 of their offering document states:

The Internal Shariah Supervision Committee of HSBC Bank Middle East Limited and the Sharia Advisory Board of Dubai Islamic Bank PJSC, Dar Al Sharia, have each confirmed that the Transaction Documents are, in their view, compliant with the principles of Sharia, as applicable to, and interpreted by, them.

In March of 2023, Air Lease, a US-domiciled airplane leasing company, issued a $600 million five-year sukuk with a profit rate (coupon) of 5.85%. Their offering document states:

The transaction structure relating to the Certificates have been approved by the Shari'a Supervisory Board of Arab Banking Corporation (B.S.C.), the Shari'a Supervisory Board of Citi Islamic Bank E.C., the Khalij Islamic, Sharia Advisor to Deutsche Bank AG, the Internal Sharia Supervisory Committee of Dubai Islamic Bank PJSC, the Internal Sharia Supervisory Board of KFH Capital Investment Company K.S.C.C.2

Once we have confirmed a sukuk's Islamic compliance, we evaluate whether the security meets our investment objectives of capital preservation and current income. This evaluation incorporates a rigorous credit review process and analysis of the security's relative value and how it will complement the overall portfolio's construction.

Amanie Advisers, a leading independent consultant specializing in Islamic finance, reviews the holdings of each Amana Fund, including the Participation Fund, on a quarterly basis to ascertain the Funds' adherence to Islamic principles. We publish their quarterly certifications on each Fund's individual page as well as on our Halal Investing page (www.saturna.com/halal).

2. Why is there performance disparity between the Amana Participation Fund and the FTSE IdealRatings Sukuk Index?

There are two reasons for the performance disparity between the Amana Participation Fund and its benchmark. The first is structural, and likely to have a long-lasting influence. The second includes dynamic attributes and reflects temporal differences in the composition of the benchmark relative to the Fund.

The FTSE IdealRatings Sukuk Index and Bloomberg Global Aggregate US Dollar Sukuk Unhedged Index are both commonly used as benchmarks for sukuk portfolios. The Amana Participation Fund uses the FTSE IdealRatings Sukuk Index as a proxy to communicate relative performance in its marketing material.

Structural Attributes

Investment performance disparity can largely be attributed to the differing objectives of the Amana Participation Fund compared to the indices. The Fund's investment objectives are capital preservation and current income consistent with Islamic principles. The objective of both benchmarks is to measure the performance of the entire global US dollar-denominated sukuk market.

Three structural attributes differentiate the Amana Participation Fund from the indices. First, the Fund is required to maintain a dollar-weighted average maturity of two to five years to mitigate duration risk, which helps reduce portfolio volatility. This allows the Fund to meet its primary objective of capital preservation. In comparison, the indices require their constituents to have maturities of one year at a minimum, and neither have limitations on maximum maturities.

Second, an index represents a hypothetical allocation, or a "paper trade," designed to simulate the underlying attributes of its holdings. Neither of the two benchmarks actually trade or own the underlying securities that constitute their respective portfolios, and therefore have no trading expenses. They also do not incur expenses related to communicating with shareowners (as they don't have any), expenses for distribution, or any other aspects of running a mutual fund. In contrast, the Amana Participation Fund must acquire securities for its portfolio, communicate with its shareowners, pay mutual fund platforms for distribution, and pay other administrative fees. Our investment team develops ongoing relationships with global and local broker-dealers. We prefer to work with local broker-dealers, some based in Dubai, as they offer valuable on-the-ground insight regarding market characteristics and details on a given issuer. These relationships are essential to providing liquidity and favorable execution on securities. Furthermore, securities are subject to the fluctuations of supply and demand, the issuer's underlying creditworthiness, the size of the offering, availability, and capital market flows.

Third, the Amana Participation Fund is limited by the US Securities Act of 1933 in purchasing newly issued securities that are "exempt from registration," also called "REG S" securities. The Fund must wait a minimum of 40 days before acquiring a REG S security in the secondary market. The benchmarks have no such limitation, as they assign hypothetical allocations but don't acquire any securities.

Dynamic Attributes

Dynamic attributes reflect temporal differences over a given period, unlike structural attributes, which have longer-term affects. Dynamic attributes include differences between the benchmarks and the Amana Participation Fund regarding geographic exposures, issuer type (such as sovereign or corporate), sector weightings, duration, and other factors.

Concentration is one dynamic attribute that distinguishes the indices from the Amana Participation Fund. At year-end 2023, both the FTSE IdealRatings Sukuk Index and the Bloomberg Global Aggregate US Dollar Sukuk Unhedged Index retained concentrated positions while the Fund had fewer concentrated positions to promote diversification to help reduce risk. The Fund's exposure to the government of Saudi Arabia, including the government-sponsored entities Saudi Electric and Aramco, was 13.65%. At the same time, the FTSE Index and the Bloomberg Index's exposures to the government of Saudi Arabia were 28.96% and 24.95%, respectively. The Fund had a 7.65% exposure to Indonesian sovereign sukuk, while the FTSE Index had a 19.66% exposure and the Bloomberg Index had a 16.93% exposure. We believe diversification is an important factor in serving our clients for achieving capital preservation and current income consistent with Islamic principles.

Dynamic attributes can also help the Amana Participation Fund achieve its investment objective of capital preservation by mitigating risk. At the onset of the pandemic, the portfolio team took proactive steps to increase the Fund's exposure to industries and sectors that were more likely to be insulated from the financial impact of COVID-19, including telecommunication firms, utility operators, and sovereign issuers. At the same time, the investment team eliminated exposures to sectors and industries that were expected to experience heightened financial duress and volatility, including air travel, real estate developers, the hospitality industry, and related tourism.

| Geographic Concentration as of year-end 2023 | |||

| Region | Amana Participation Fund | FTSE Ideal-Ratings Sukuk Index | Bloomberg Global Aggregate US Dollar Sukuk Unhedged Index |

| Saudi Arabia (Sovereign) | 5.98% | 19.75% | 15.97% |

| Saudi Arabia GSEs (SECO & Aramco) | 7.67% | 9.21% | 8.98% |

| Saudia Arabia (Comprehensive) | 13.65% | 28.96% | 24.95% |

| Indonesia | 7.65% | 19.66% | 16.93% |

| Total | 21.30% | 48.62% | 41.88% |

3. What does it mean if an issuer is non-rated? How prevalent is this rating among sukuk issuers?

Typically, issuers hire the major credit rating agencies, including Moody's Investors Service, S&P Global Ratings, and Fitch Ratings, to provide credit ratings for their securities. Bonds and sukuk broadly fall into three credit rating categories: investment-grade (IG), high-yield (HY) and non-rated (NR).

Investment-grade issuers will obtain a credit rating that falls within a range of AAA to BBB (AAA, AA+/-, A+/-, BBB+/-) where AAA represents the highest rating and BBB is the lowest. The plus or minus denotes if the issuer is on the higher or lower range of its tranche. Securities that obtain investment-grade ratings typically demonstrate financial strength, sufficient free cash flow from operations to provide ongoing liquidity, and the capacity to meet their financial obligations to sukuk holders or bondholders. A higher investment grade doesn't necessarily mean that an issuer won't default, but it does mean that the credit rating agency believes default is less likely.

A high-yield issuer will obtain a credit rating that falls within a range of BB to D (BB+/-, B+/-, CCC+/-, CC+/-,C+/-, D) where BB is the highest rating and D is the lowest, meaning that the issuer is in default. These issuers tend to exhibit less robust financial strength, resilience, and cash flow generation when compared to investment-grade issuers.

If an issuer is non-rated, it simply means the issuer has not obtained a credit rating from a well-recognized agency. Typically, investors require non-rated issuers to offer debt or sukuk with a higher yield, or profit, to compensate for the perceived higher risk. Other factors that can affect an issuer's bond yields and the profit rate for sukuk include offering size, perceived liquidity, management's reputation, the issuer's industry and sector, existing debt or leverage, and the issuer's history of operation. The list of factors is extensive and is continuously evolving. Attention to an issuer's financial standing, along with its trajectory, is a vital part of our ongoing due diligence process.

Each issuer determines whether they want to obtain a credit rating. It is worth noting that sometimes cultural characteristics can influence whether an issuer wants to obtain a credit rating. This is common among emerging market issuers. For example, the emirate of Dubai and many of its related government entities have opted to not obtain a credit rating even though it is likely they would be graded favorably.

A shared assumption among the investment community is that Dubai's hesitance to obtain a credit rating is to avoid comparison with their neighbor, Abu Dhabi, which as of writing retains a credit rating of AA. Dubai's implied credit rating in the eyes of the investment community is assumed to be somewhere in the BBB range – a considerable step below that of Abu Dhabi.

This implied difference is something that the government of Dubai may not want to formalize, preferring to keep its rating undefined. Note that this is not an official rationale, but rather an assumption shared among the investment community.

4. Can the Fund invest in non-US dollar-denominated sukuk? What is your philosophy on investing in these securities?

In short, yes. However, the Amana Participation Fund restricts its investments so that at least 50% are denominated in the US dollar as measured by the Fund's assets under management, with no more than 10% in any other single currency.

While the Amana Participation Fund is permitted to invest in non-US dollar-denominated securities, the portfolio management team's current bias is to retain a US dollar focus. The incorporation of non-US dollar-denominated securities into the portfolio may introduce an additional layer of risk that could detract from the Fund's investment objectives. Furthermore, the Fund's investor base is US-domiciled and the portfolio management team currently is inclined to retain a currency bias consistent with the base currency of its clients.

The investment team has explored owning currencies pegged to the US dollar. Among these are the Saudi riyal (SAR) and the United Arab Emirates dirham (AED). The potential benefit of owning currencies pegged to the US dollar is that it greatly reduces currency risk – the exchange of value of one currency (domestic) into another (foreign) and then back again into the currency of the country of the investors' domicile.

Non-US dollar-denominated sukuk can sometimes offer higher profit rates in their local currency markets, which can be appealing, but several factors need to be taken into consideration. While rare, currency pegs can and do break. A broken currency peg means that the related currency exchange is no longer fixed at the original exchange rate, but becomes free-floating or adjusted, usually downward, to the disadvantage of investors. Other factors include taxes incurred on foreign investors, custody of local currency securities, and liquidity. Once these factors have been taken into consideration, the perceived higher profit rate offered in the local currency may diminish.

The Amana Participation Fund's investment team routinely reviews market conditions to determine whether an allocation to a non-US dollar security makes sense from a risk-return perspective. We don't want to rule out the possibility that such an endeavor will not occur; however, we are mindful to balance the risk with the potential return.

5. Why does the Fund have a large geographic exposure to Middle Eastern issuers? How large is the sukuk market?

Middle Eastern issuers dominate the US dollar-denominated sukuk market. The Amana Participation Fund primarily invests in the six countries of the Gulf Cooperation Council (GCC), a political and economic alliance in the Arabian Peninsula. Its members include Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE). The GCC was established in 1981 to promote security and stability for its members.3 The population of the GCC as of year-end 2022 was over 56 million, representing just 0.7% of the global population.4 The countries of the GCC generate 2.2% of global gross domestic product (GDP). However, 32.8% the world's oil supply comes from the GCC region, which gives these countries significant influence on the world stage.

As of writing, sukuk have been issued in 27 different currencies around the world. Malaysian ringgit has the largest share of the market, representing 47% of global issuance from year-end 2000 through year-end 2022. US dollar-denominated sukuk is the next largest group, representing 22% of global issuance, and Saudi Arabian riyal-denominated sukuk represents 10%. By year-end 2023, the total volume of outstanding global sukuk was over $850 billion, exceeding the size of the eurodollar's high-yield market by nearly $100 billion. The sukuk market is anticipated to reach over $1 trillion in the near-term future.5

GCC issuers have largely dominated US dollar-denominated sukuk issuance since 2017. The GCC region represented 54.5% of global sukuk issuance in 2023, above its three-year average of 41.9%, which was skewed downward because GCC issuance had lower representation in 2022 of 28.1%. The reduction in issuance in 2022 can be partly attributed to high hydrocarbon prices and the region's governments engaging in fiscal consolidation; sovereign debt-to-GDP metrics declined and the budget deficit for some countries was reversed.

Supranational entities, such as the Islamic Development Bank (IsDB), were the second largest issuer of sukuk in 2023. Such issuers represented 27.1% of total issuance, down from its three-year average of 36.8%. The third largest issuer was Turkey at 5.9% and the fourth largest issuer was Indonesia at 3.7%.

| US Dollar Sukuk Issuance Trends (2010 - 2023) | |||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

| Total Islamic Issuance ($ bn) | 9,415 | 18,536 | 18,450 | 28,560 | 21,093 | 32,435 | 38,783 | 33,846 | 38,724 | 45,291 | 49,364 | 37,249 | 58,084 |

| Change in % | 96.9% | -0.5% | 54.8% | -26.1% | 53.8% | 19.6% | -12.7% | 14.4% | 17.0% | 9.0% | -24.5% | 55.9% | |

| Regionalized Summary US Dollar Sukuk Issuance Trends (2010 - 2023) | |||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

| GCC | 56.5% | 75.8% | 61.0% | 36.7% | 28.5% | 35.1% | 49.5% | 51.4% | 52.8% | 48.8% | 43.0% | 28.1% | 54.5% |

| Supranational | 8.0% | 8.6% | 14.5% | 36.4% | 38.9% | 35.3% | 33.7% | 33.2% | 32.4% | 36.9% | 38.3% | 44.9% | 27.1% |

| Asia (Includes Pakistan, India, & Maldives) | 31.9% | 7.3% | 12.5% | 15.1% | 31.4% | 23.5% | 13.2% | 12.3% | 6.7% | 6.6% | 12.0% | 12.2% | 8.3% |

| MENA excluding GCC members | 3.7% | 8.1% | 11.9% | 8.2% | 1.2% | 5.7% | 3.5% | 1.5% | 5.8% | 5.5% | 6.2% | 14.8% | 8.5% |

| Europe | 0.0% | 0.2% | 0.1% | 0.1% | 0.0% | 0.3% | 0.0% | 1.6% | 2.4% | 2.2% | 0.5% | 0.1% | 0.6% |

| Other | 0.0% | 0.0% | 0.0% | 3.5% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 1.0% |

| 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | |

| GCC & Supranational (only) | 64.4% | 84.4% | 75.5% | 73.1% | 67.4% | 70.4% | 83.3% | 84.6% | 85.1% | 85.7% | 81.2% | 73.0% | 81.6% |

6. What are the most common types of sukuk? Does the type of sukuk structure affect its credit rating?

The sukuk market has come a long way since the first corporate sukuk issuance in 1990 by Shell MDS Sdn Bhd, the Malaysian subsidiary of the former energy company Shell Corporation, for 125 million Malaysian ringgit.6 It would be another 11 years before the Bahrain Monetary Authority (now the Central Bank of Bahrain) would present the first government-backed sukuk.7 As of year-end 2023, the total volume of outstanding international sukuk across all markets and currencies was in excess of $850 billion,8 with forecasts for total issuance to exceed $1 trillion in the near future.9

The International Islamic Financial Market (IIFM), a global standard-setting body of the Islamic Financial Services Industry (IFSI), tracks the evolution of sukuk markets and the preferences of issuers and investors.

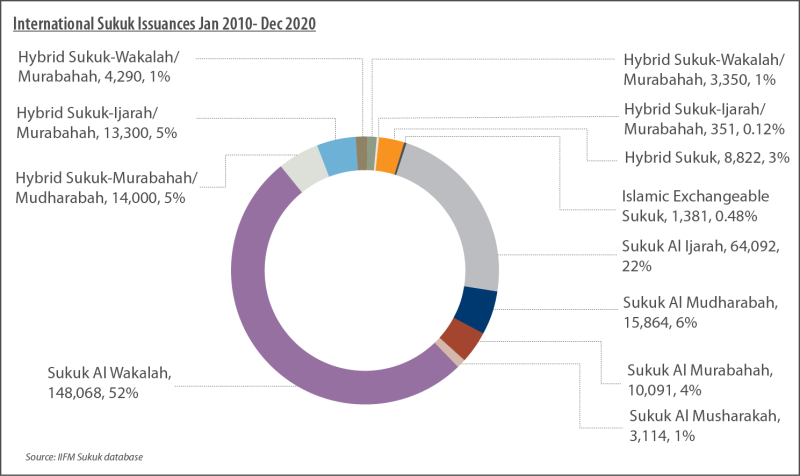

The IIFM's 2023 annual report identified 12 types of sukuk structures. For the 10-year period ended December 2020, three sukuk structures accounted for 80% of total issuance. Sukuk al wakalah represented 52% of issuance, sukuk al ijarah represented 22%, and sukuk al mudarabah (ijarah/murabahah) represented 6%.10

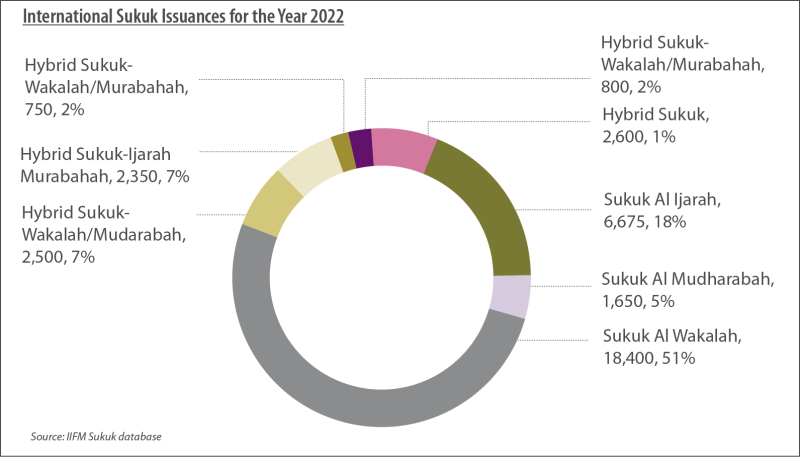

Issuers can also offer hybrid sukuk structures, which promote flexibility and substitutability of the assets assigned to the certificate, if needed. A hybrid sukuk structure can also help the issuer ensure that the certificate meets eligibility parameters of certain benchmarks, such as the JPMorgan Emerging Market Bond Index (EMBI). As of year-end 2022, four sukuk structures represented 84% of total issuance; sukuk al wakalah represented 51%, al ijarah represented 19%, and hybrid sukuk ijarah/murabahah and murabahah/mudarabah each represented 7%.11

The universe of sukuk structures is far more extensive than what is typically issued in international markets. However, just a few types of sukuk have become the most frequently issued, reflecting both issuer and investor preferences regarding documentation and flexibility of the structure.

The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) defines sukuk as "certificates of equal value representing undivided shares in ownership of tangible assets, usufruct, and services or (in the ownership of) the assets of particular projects or special investment activity."12 Sukuk can be divided into four types based on the structure: asset-backed, asset-based, hybrid, and exchangeable.

An asset-backed sukuk is an Islamic certificate backed by underlying assets financed by investors to obtain Islamic-compliant income. The issuance of an asset-backed sukuk can either be on or off the issuer's balance sheet.13 From a structural standpoint, the underlying assets are typically transferred to a special purpose vehicle (SPV) and the issuer transfers full legal ownership of the assets to the investors. The SPV then issues a certificate to the investors, which represents an undivided ownership in the underlying assets. This sukuk type is al-ijarah, which exhibit the characteristics of a sale-leaseback structure. The sukuk's credit rating can be influenced by the characteristics of the underlying assets, which may include real estate and other tangible assets. However, credit ratings are generally more dependent upon the issuer's creditworthiness rather than the underlying assets because the issuer typically repurchases the certificate from the investors upon maturity.

For an asset-based sukuk, investors have a beneficial ownership interest rather than a real ownership interest, usually retained on the issuer's balance sheet.14 This beneficial ownership interest is attained through the assets held in an SPV. It is common for asset-based sukuk to include intangible assets. The list of asset types is extensive, but they must all be Islamic-compliant. Islamic banks commonly issue asset-based sukuk. Given this type of structuring, asset-based sukuk are often viewed as unsecured and it is common for the sukuk to retain a pari-passu (equal treatment) ranking in the issuer's capital structure. Because of the unsecured status and the issuer's obligation to repurchase the certificate upon its maturity, the credit rating of an asset-based sukuk is typically dependent upon the creditworthiness of the issuer.

The rationale for a credit rating being assigned to an issuer, rather than the underlying assets, reflects the obligation of the issuer upon the certificate's maturity. When sukuk reach maturity, the issuer buys them back through a purchase undertaking agreement (PUA). The terms of the PUA can vary based upon the issuer's prospectus. The issuer is obligated to return the investors' principal along with any undistributed profit. The issuer must produce the funds needed to repurchase the certificate. Typically, the issuer will employ similar tactics that conventional debt issuers might use for financing. Issuers may use funds from cash held on their balance sheet or raise additional funds in the capital markets prior to the maturity of the sukuk. Credit rating assignments based upon a sukuk structure may have some influence; however, the issuer's creditworthiness and their capacity to meet the terms of the PUA have a larger impact.

Issuers began selling hybrid sukuk to address investor preferences and to provide some flexibility to sukuk structures. With this structure, a prospectus will include a substitution clause, permitting the issuer to exchange the underlying assets used to generate the sukuk's income. This allows the issuer to change the composition of the underlying assets tethered to the certificate if they are not performing as expected. There can be many reasons an issuer may change the composition of the underlying assets. The inclusion of substitution language in a prospectus is common among most issues. Ultimately, this helps promote the creditworthiness of the sukuk.

Hybrid sukuk can be sized to accommodate investor preferences. Investors typically prefer issuance in round sizes, such as $500 million or $1.0 billion tranches. Issuance of sukuk in these sizes typically meet benchmark eligibility requirements that can improve investor demand and subsequent liquidity. This can help the issuer with the substitution process as it allows greater flexibility in the types of assets (e.g., both tangible and intangible). In 2015, Emirate Airlines issued a 10-year sukuk, guaranteed by the UK's export-finance agency, to fund the acquisition of four Airbus A380-800s for $913 million.15 In the event Emirates Airlines needed to substitute one or more of the airplanes used to back the sukuk, the company may be hard-pressed to find a substitute airplane with a valuation that would fit within a $913 million certificate size. A hybrid sukuk structure would allow a combination of asset types, up to a predetermined percentage of the asset base.

As of writing, two different hybrid sukuk types are the most popular in the market – al ijarah/murabahah and murabahah/mudarabah.

Lastly, an exchangeable sukuk has an embedded option that gives the holder the right to convert their ownership interest into an asset without obligation. Such sukuk have a schedule that predetermines the conversion at some future date. In most circumstances this type of sukuk permits the holder to convert ownership into stock or some other predetermined asset. This type of sukuk is rare.

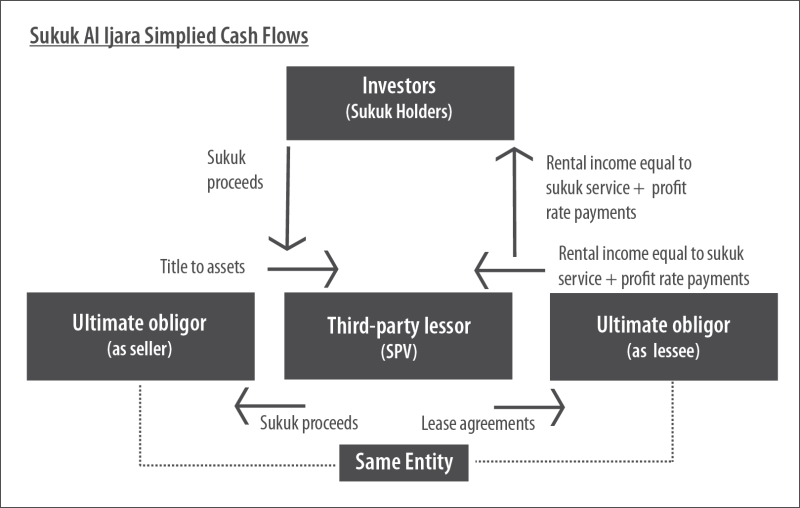

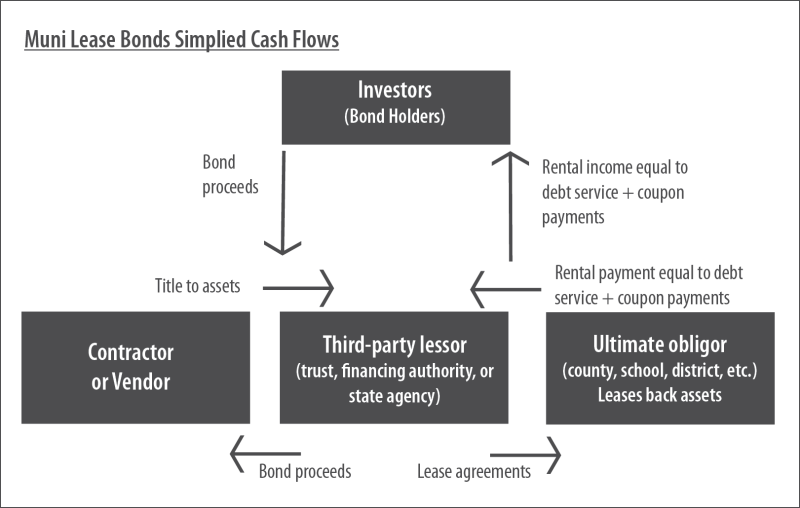

7. In what ways are sukuk similar to municipal appropriation bonds?

The cash flow structure for sukuk al ijara shares some similarities with that of a municipal bond. Typically, both types of securities utilize a lease financing structure, and the assets are placed in a trust. For sukuk, assets are placed in a special purpose vehicle (SPV). For municipal securities, assets are placed with a third-party lessor such as a trust or local financing authority. In both cases, the ultimate obligor submits payments to the trust holding the assets that equal the debt service obligations, which ultimately flow toward the investors.

Muni Certificate of Participation Structure

For municipalities, lease financing is typically used when a local government wants to finance the construction of a new building. The title to the assets is transferred to a third-party lessor, usually a trust, a financing authority, or a state agency. When investors buy the bonds, the proceeds go to the third-party lessor and are used to finance the construction of a building. The ultimate obligor then leases back the assets and sends payments to a third party equal to the debt service, which flow onward to the bondholders.

Sukuk Structure

Sukuk al ijiara are basically structured as finance leases. The title of assets is transferred to a third-party lessor, the SPV. The ultimate obligor pays rent to service the obligations through profit distributions, which then flow to sukuk certificate holders. The main difference is that the ultimate obligor is both the seller and lessee.

Sukuk are structured with similar cash flows to municipal certificates of participation.

| Muni Lease Bonds | Sukuk | |

| Structure | Ultimate obligor pays lease payments to a third party equal to debt service, which then flows to investors covering coupon and debt service | Ultimate obligor pays lease payments to a third party that satisfies the rental obligations, which then flows to investors as part of the profit rate (coupon) and sukuk service |

| Issuing Entity / Third Party | Can be a state agency, public financing authority, or trust | Generally an SPV |

| Coupon / Maturity | Has a stated maturity and coupon payments | Has a stated maturity and coupon payments, referred to as "profit rates" or "return" |

| Use of Funds | Usually finances the contruction of a facility | Can include more general financing needs |

| Substitution of Underlying Assets | Yes, in some cases — especially in California | Generally yes |

| At Maturity | Ultimate obligor typically acquires assets upon maturity | Ultimate obligor acquires assets upon maturity, funding a principal return, typically a "purchase undertaking" |

| Additional Security | Can include a pledge of collateral | Can include a negative pledge |

8. What is your investment process?

Our investment process includes both a top-down macroeconomic outlook and a bottom-up investment approach, integrating a deep, credit-driven review with a relative value framework.

We begin our investment process by assessing the macroeconomic environment and how the market priced in expectations about economic growth, inflation, and interest rates. This helps us to construct and position a portfolio. Our group takes a long-term strategic view while recognizing that, at times, tactical adjustments may be needed regarding the outlook on interest rates and other important economic factors.

While Islamic-compliant securities, such as sukuk and murabaha, are not interest-bearing instruments, they are sensitive to changes in conventional, interest-bearing securities. We look to both Islamic-compliant and conventional fixed-income markets when positioning portfolios.

Portfolio Positioning

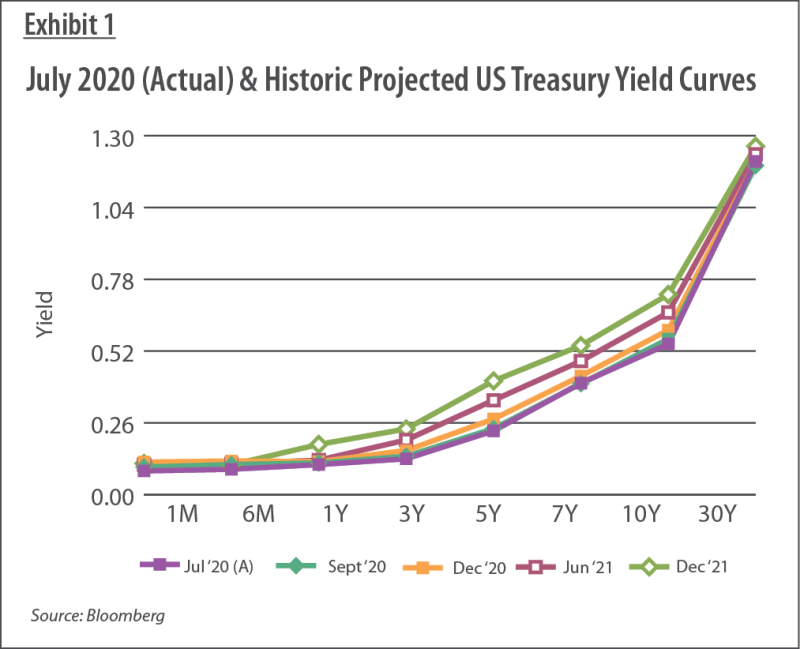

In July of 2020, we used the forward interest rates markets to make economic growth projections over the upcoming 18 months. Exhibit 1 details the forward yield curve, or investors' expectations in the changes of future yields, from July 2020 through December 2021.

While these may be just ranges of projections, they relay vital information on how different market participants adjust to revised forecasts regarding inflation, economic outlooks, and market sentiment along varying parts of the yield curve. At the time, these forecasts reflected underlying contracts indicating market participants were deploying large sums of capital in attempt to offset risk, lock in funding obligations, and make other important capital markets decisions.

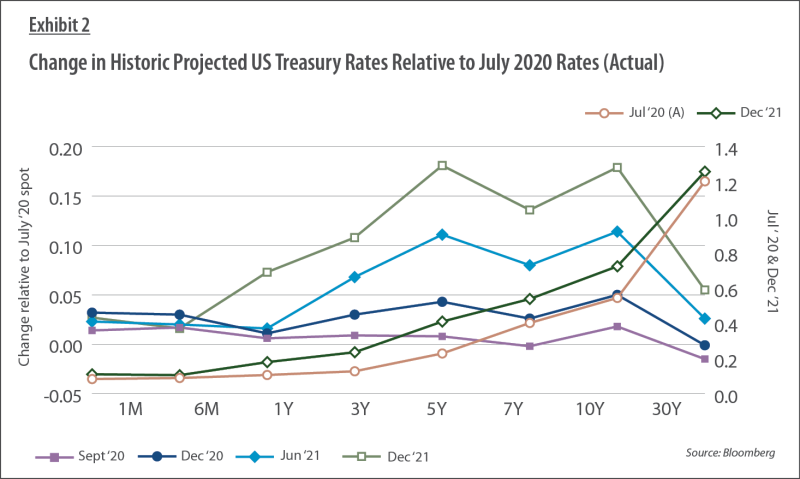

Exhibit 2 details the expected change in interest rates when compared to the spot rate as of July 31, 2020. On that date, rates were projected to decline across the entire yield curve except in June 2021 and December 2021. These interest rate movements along the yield curve likely reflect an extended period of anemic economic growth, and with it a lower interest rate environment. We also inferred mild interest rate volatility among long-term maturities. Given these projections, we believed that the Federal Reserve's emphasis on "lower for longer" would result in lower short-term interest rates that would most likely flatten out the short end of the yield curve up to the five-year maturity. This prediction was consistent with current market observations; the yield of the five-year US Treasury fell to a historical low of less than 20 basis points (bps) during the first week of August 2020.

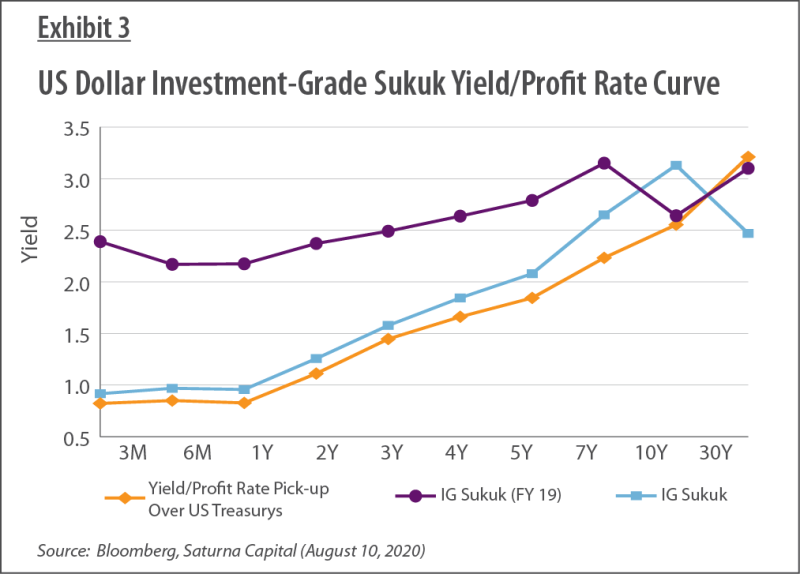

To determine positioning and relative value, we used the shape of the US dollar sukuk yield curve. In Exhibit 3, US dollar investment-grade sukuk retained a favorable pick-up over US Treasurys throughout the entire yield curve. US Treasury yields are not included in Exhibit 3 but rather investment-grade sukuk for year-end of 2019 and August 10, 2020. The orange line shows the yield/profit rate enhancement that investment-grade sukuk earn above US Treasurys throughout the yield curve. Investment-grade US-dollar global sukuk, on average, retained approximately a 75-bps yield/profit rate pick-up over US Treasurys with a duration of less than one year. For maturities between three and five years, the yield/profit rate pick-up was over 150 bps. For maturities of seven years or more, the yield/profit rate pick-up was well over 200 bps. Exhibit 3 includes the yield/profit rate of the US dollar investment-grade sukuk at year-end 2019 to show how the curve has changed.

Holding US dollar-denominated investment-grade sukuk retains considerable return enhancement over US Treasurys. Positioning in the one-to-seven-year buckets can offer value even if they experience mild volatility.

Based upon our analysis, experience, and outlook on the interest rate environment, we used a yield curve positioning strategy that incorporates a barbell approach for the deployment of new investments. A barbell strategy focuses on allocating capital among issuers with either short or long-term maturities while avoiding intermediate maturities. The barbell strategy neutralizes the portfolio against small parallel shifts (equal upward or downward interest rate movements) of the yield curve, yet intentionally exposes the portfolio to portions of the curve that are anticipated to outperform, such as the long-term maturities. This strategy positions the portfolio where we anticipate optimal performance, but still has exposure across the curve to mitigate risk while retaining sufficient short-term instruments to provide flexibility.

Bottom-Up Process

Our bottom-up process is driven by Saturna's relative value process, which systematically tracks the spreads of the universe of sukuk issuers in conjunction with credit research. In both fixed income and equity issue analysis, Saturna's portfolio management team has local on-the-ground experience that provides industry and regional coverage. We collaborate with each member's assessment of issuers based upon assignment of industry and sovereign coverage.

Emerging market economies tend to be characterized by idiosyncratic conditions and characteristics that typically differ from the more efficient markets as observed in developed economies. We seek competitive returns relative to our benchmark and among our competitors through a multi-pronged approach. This approach includes our on-the-ground experience, network of relationships with the issuers and local brokers, a deep understanding of the community and respective cultures, and intimate knowledge and tracking of macroeconomic and industry drivers, complemented by deep credit analysis which integrates a relative value framework.

Our process for seeking competitive returns means conservatively positioning the portfolio among issuers with robust balance sheets, strong credit ratings, and resilient cash flows, led by experienced and prudent management teams. This is a core pillar of Saturna Capital's investment philosophy and is consistent with tenants of Islamic-compliant investment principles.

We do not believe that it is possible to consistently create a competitive advantage relative to the benchmark and to our competitors by anticipating changes in the yield curve through duration-based allocations. We do, however, seek to position the Amana Participation Fund to compete in all market conditions. Our focus on generating competitive income and risk-adjusted returns for investors is better served by owning higher quality issuers that are better positioned to endure the business cycle and unexpected geopolitical and external shocks, such as the onset of wars or the pandemic. As such, our clients have been favorably served by our prudent active management process that focuses on quality and conservatism. Our aim is to be stewards of our clients' investments through our efforts to provide capital preservation and current income.

Relative Value:

Saturna Capital has extensive experience in identifying issuers through a relative value process that selects favorable investment return opportunities compared to its peer group. This helps us to achieve our investment objectives of capital preservation and providing Islamic-compliant income. We find the relative value process helps identify potential investment candidates that trade cheaply based upon their history. Securities can trade at wider spreads relative to their peer group due to deteriorating credit metrics or other issues that may relate to the issuer's business activities. Sometimes these pricing anomalies are due to changes in investor sentiment or rebalancing led by large institutional firms. Ultimately, there can be a host of other external factors that may cause a change in pricing. Our relative value framework, in conjunction with our extensive credit analysis and relationships with issuers and local broker-dealers, provides valuable context to determine whether a change in pricing signals an opportunity or potential risks. As a result, the relative value framework is a credit-driven process that aims to optimize the portfolio's capital allocation among issuers that are trading at cheaper valuations.

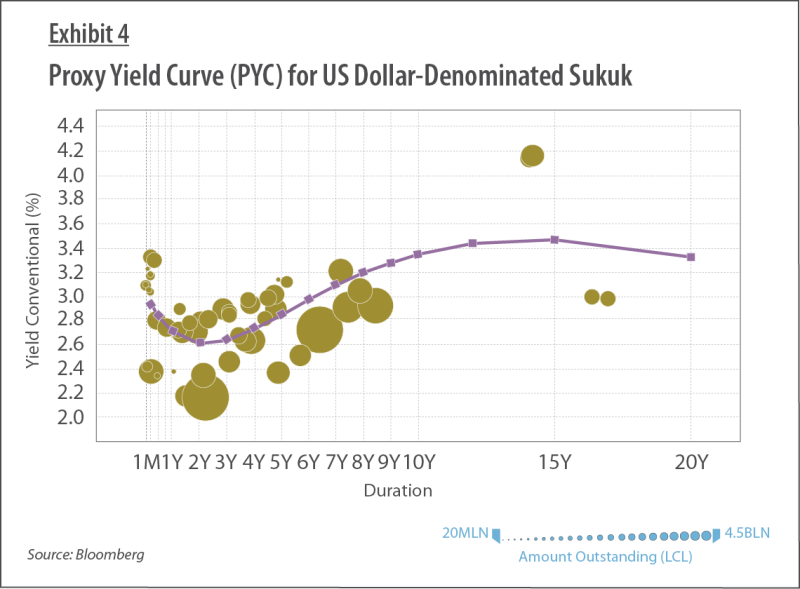

Exhibit 4 depicts a proxy yield curve (PYC) for US dollar-denominated sukuk with an A+/- credit rating to identify a relative value framework. The PYC identifies securities that may be overpriced, which are positioned below the PYC, or it may indicate that an issue is trading cheaply on a historical basis, which is positioned above the PYC. This process can be extended further into credit rating, duration, or industry.

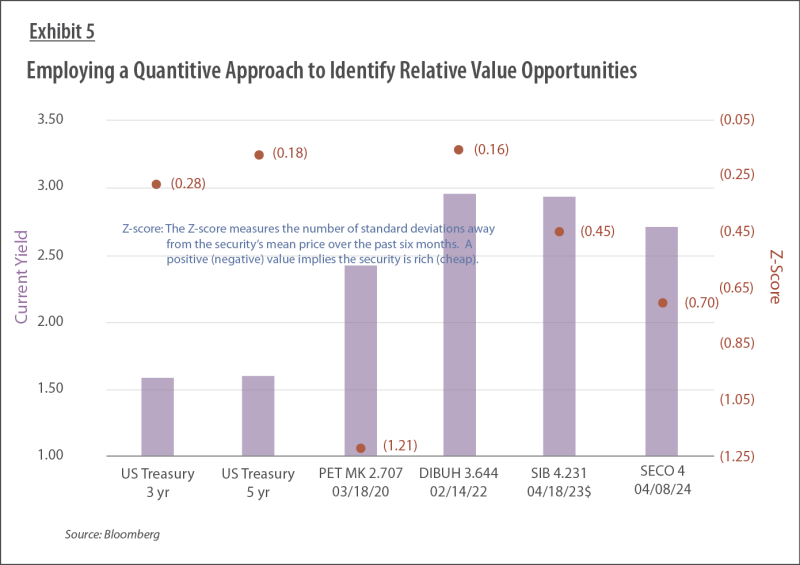

Our relative value assessment then reaches the individual security. At this level, securities are compared with their historical performance to identify potential value using their z-score, which is a measure of standard deviations above or below a security's average price during a specified period. Exhibit 5 shows an example of the z-scores of four A-rated sukuk, with durations from three months to 4.25 years, over a trailing six-month period. US dollar-denominated global sukuk have been trading at richer valuations relative to the prior two years, in part due to their inclusion in the JPMorgan EMBI Index and the GCC region's strong credit ratings, which offer a favorable yield enhancement over US Treasurys.

To sum up, our process offers a threefold benefit for the management of the portfolio. First, it helps us identify when a desired security is overpriced or cheap based on its previous trading history. Second, the framework helps us identify new investment candidates for credit review that can be placed on our watch list for potential inclusion in the portfolio as we wait for opportunistic pricing. Third, the process offers context to help us position the portfolio throughout a business cycle. Issuers in a collective industry tend to exhibit similar price behaviors, trending from cheap to overpriced, and then trending back to cheap.

In addition to a top-down macroeconomic assessment and a bottom-up process of determining relative value, we also incorporate stress testing on the portfolio. The purpose of stress testing is to help us understand how the portfolio may move under hypothetical changes in interest rates or potential external shocks so that we can evaluate any potential weaknesses.

9. What criteria would cause you to sell sukuk?

Our bias is to hold on to a security and closely track its financial performance through a business cycle. However, there are certain conditions that would motivate a sale. If we identify fraud or a substantive change in management's strategy that we believe could impair its financial resilience down the road or weaken its ability to protect sukuk holders' interests, we would choose to sell.

There are also less dire conditions in which we may choose to sell a sukuk; for instance, for the availability of a swap. A swap refers to the selling of one sukuk, then using the proceeds to acquire another sukuk from the same issuer. The rationale is that the issuer may come to the market to issue a new sukuk with a longer maturity that better matches the desired portfolio attributes that we seek. Sometimes the security sold is overvalued, whereas the new sukuk is cheaper than its peers. We engage in this process on an infrequent basis. Such actions are taken with the goal of enhancing the portfolio's return profile while keeping a keen eye on risk.

10. How does your team mitigate risk?

Saturna Capital strives to mitigate risk while being stewards of our clients' investment capital. There are a variety of internal processes and policies that we employ to reduce risk.

The Amana Participation Fund's prospectus states that the Fund is non-diversified and may invest a larger percentage of assets in fewer issuers. We will note that we actively seek to mitigate risk by diversifying among geographies, sectors, and industries when appropriate. However, this Fund will likely retain a heavy concentration among GCC issuers. The Islamic community tends to retain a regional concentration in Southeast Asia and the Middle East. Typically, sukuk are issued by Muslims for those seeking Islamic-compliant investments. We will note that this market is evolving and does occasionally attract issuers from Europe, the US, and other non-Muslim countries. Due to issuer geographic concentration we do not have limits on industries or sector weightings.

We also believe it is important to address the liquidity profile of the US dollar-denominated sukuk market and the Amana Participation Fund. Our group incorporates regular liquidity assessments of the securities held in the portfolio. Before we outline these procedures we believe that it would be helpful to frame our regulatory environment by offering an overview.

The Securities and Exchange Commission (SEC) has several rules and regulations that address liquidity for mutual funds registered under the Investment Company Act of 1940 (The '40 Act). These rules aim to ensure that funds have sufficient liquid assets to meet redemption requests from investors without significantly impacting the fund's net asset value. Rules regarding liquidity are governed, in part, by Rule 22e-4: Liquidity Risk Management Programs:16 The rules include the following:

- Each fund must adopt and implement a written liquidity risk management program.

- The program must assess and manage the fund's liquidity risk, including:

- Classification of portfolio investments based on liquidity (e.g., highly liquid, moderately liquid, less liquid, illiquid).

- Determining and periodically reviewing a minimum percentage of the fund's net assets that must be invested in highly liquid investments.

- Limiting the fund's investment in illiquid assets.

- Implementing policies and procedures for managing redemption requests.

It is important to define what we mean by "highly liquid" and "moderately liquid." For a security to be deemed highly liquid, the fund manager reasonably expects the security to be convertible into cash in current market conditions within three business days without the conversion significantly changing the market value of the investment. A moderately liquid security is likely to take more than three but fewer than seven business days to be converted into cash without significantly changing the investment's market value. While the liquidity profile of securities held can change, the fund manager has historically deemed the securities of the Amana Participation Fund to be highly liquid.

Since '40 Act funds are regulated investment pools by the SEC, an open-end fund must adhere to the regulatory framework to include the liquidity profile of the fund. The Amana Participation Fund offers daily liquidity to all of its investors without limitation on the size of their redemption.

Regarding potential risks, the Amana Participation Fund is unleveraged, which is consistent with Islamic principles. The Fund does not short securities, trade on margin, or offer securities for lending. The Fund is permitted to invest in non-US dollar-denominated securities; however, we have opted not to do so.