Fixed Income Markets Q3 2025 Commentary

Key Market Takeaways

- Inflation and labor market trends have diverged: inflation has risen (around 3%), driven mainly by services, while the labor market has slowed and the Fed is weighing difficult policy decisions.

- Tariff effects on prices have mostly impacted businesses so far, but these may eventually be passed on to consumers, especially hurting lower-income groups.

- Markets remain strong, with risk assets and gold performing exceptionally well, driven by global liquidity, resilient economies, and AI optimism, even as recession forecasts have failed to materialize.

The third quarter of 2025 was defined by three key themes: rising domestic inflation, a slowing labor market, and global risk asset excellence amid extensive geopolitical tension.

Ahead of President Trump’s early-2025 aggressive tariff regime, the US price landscape was precarious. Sticky shelter costs prohibited a lack of a clear move toward the Federal Reserve’s 2% inflation target, while domestic uncertainty and low energy prices added to apprehension. As tariff policy became clearer, expectations of a sharp uptick in goods inflation emerged, and debates were plentiful regarding whether any tariff-driven price increases would be a one-off or if price pressures would persist for longer.

Over the summer, we saw various measures of inflation bounce from their second quarter lows and move toward 3%, but the drivers of the inflection were unexpected. Instead of a highly anticipated resurgence in core goods inflation, services inflation remained the top contributor, with core good inflation showing only a modest uptick so far. We can attribute these unique dynamics to a few primary factors:

- The US economy has remained far more resilient than expected on the back of strong consumption and private fixed investment. US consumption is dominated by services, and the combination of positive, albeit slowing, real wage growth and a lower savings rate has translated to resilient consumer spending and higher services prices. At the same time, excessive capital expenditure from hyperscalers and other businesses adjacent to artificial intelligence (AI) have added a marginal tailwind to the US growth outlook.

- Global energy prices have stayed lower than expected as US oil production has reached record highs and OPEC+ supply has continued to grow.

- The brunt of the tariff-driven price impact on goods has been borne by businesses and middlemen, easing the burden on the consumer.

- Shelter pricing has been experiencing disinflation from elevated levels, but the pace of disinflation is sluggish as constraining home prices and interest rates continue to lock up the housing market.

This presents a complex picture and will force tough choices for the Federal Reserve. The resilient consumer-driven economy would argue for holding rates steady, as cuts could fuel further price pressures and potentially cause a de-anchoring of inflation expectations to the detriment of the American consumer. There is also a reasonable potential for a rebound of global energy prices, particularly given the fickle standing of key relationships with Russia and the United States’ alienation of its top economic partners.

Additionally, businesses and middlemen will eventually begin to pass on tariff-driven price increases to consumers. This shift would disproportionately impact lower-income consumers — a constituency that has already been walloped by the post-COVID inflationary surge, as this demographic spends a noticeably higher proportion of their income on necessity items that have experienced massive price increases.

At the same time, a lowering of the Federal Funds Rate, if perceived as “justified” by the market, could help lower borrowing costs priced off the US 10-Year Treasury yield. Given lower long-term treasury yields, a resulting decline in mortgage rates would unlock considerable demand in the housing market, while easier access to capital may incentivize builders to take on more projects with lower hurdle rates.

Despite inflation’s failure to move credibly toward the Federal Reserve’s 2% target, the Federal Open Market Committee (FOMC) decided to cut rates 25 basis points to 4%–4.25% during their September meeting, the first reduction since December 2024. The decision was almost unanimous, with the newly appointed member Stephan Miran dissenting in favor of a larger 50 basis point cut.

During the press conference, Chairman Jerome Powell acknowledged the recent slowing of the labor market, ultimately relaying the Fed’s heavier weight on the employment side of their dual mandate. Powell dubbed the decision as a “risk management cut,” conveying a preference to preempt further labor market deterioration even if the result is an economy that is running hot. Looking ahead, the picture is no so clear. The committee is roughly split between participants forecasting two-plus cuts and participants forecasting fewer than two cuts in 2025, most of whom expect that the current rate will be maintained for the remainder of the year.

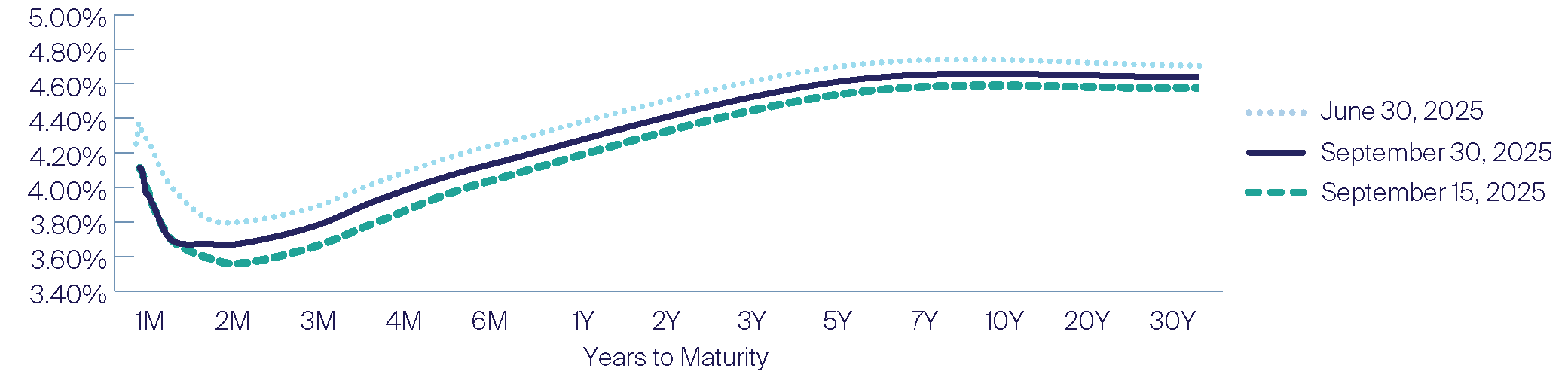

Throughout 2025, the bond market has experienced a pronounced “steepener,” a term used to describe a yield curve that steepens as short-end yields fall more than long-end yields. Notably, this trend continued through the third quarter until the mid-September FOMC meeting. The initial reaction to the FOMC decision was a steepener, but as markets digested the cut, the fixed income market marked a bear flattener, and the bond market gave back some of its previous gains.

United States Treasury Benchmark Curve

Interestingly, this market action was reminiscent of September of 2024, where the long end of the bond market sold off in response to the FOMC’s 50-basis-point cut before ultimately stabilizing. A rangebound long end through the end of 2025 is a likely scenario as the market weighs higher growth data, higher inflation, and immense fiscal expenditure, contrasted by labor market weakness, rate cuts, and solid demand for longer-term issuance.

Since 2023, many market prognosticators have forecast a recession that has yet to come to fruition. During this time, risk assets have soared, with US equity indices continuing to break all-time highs, credit spreads near historic lows, and many riskier emerging market equities and debt receiving solid capital flows. Not all investors are leaning into the financial market rally and instead are seeking returns and stability elsewhere. Gold, an asset characterized as a defensive hedge due to its typically low correlation to financial assets, is on track for its best single year in decades, returning 45% year to date.

This unusual “everything rally” can be partially attributable to a rising tide of global liquidity, supported by central bank easing, a falling US dollar, and treasury issuance patterns pushing systemic financial leverage higher. It can also be explained by the anticipated productivity surge from AI, or surprisingly resilient economies following a global tightening cycle, or shifting investor preferences. We can always find a way to justify market movements after the fact, but it is an imperfect science, and hindsight is always easier than forward omniscience.

During periods of market excellence and euphoria, it is worth taking a moment to revisit the pillars of our investment philosophy that are crucial during the best of times and the worst of times: diversify among quality issuers, focus on prudent management of risk, and temper a reactionary mindset. These principles will continue to drive our investment framework, improving our resiliency to any boom or bust ahead.

Important Disclaimers and Disclosures

This publication should not be considered investment, legal, accounting, or tax advice, or a representation that any investment or strategy is suitable or appropriate to a particular investor’s circumstances or otherwise constitutes a personal recommendation to any investor. This material does not form an adequate basis for any investment decision by any reader and Saturna may not have taken any steps to ensure that the securities referred to in this publication are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the publication.

The information in this publication was obtained from sources Saturna believes to be reliable and accurate at the time of publication.

All material presented in this publication, unless specifically indicated otherwise, is under copyright to Saturna. No part of this publication may be altered in any way, copied, or distributed without the prior express written permission of Saturna.