Navigating Inflation Shocks and Policy Shifts

Key Market Takeaways

- Supply-driven energy shocks pushed headline inflation higher in Q2 2026, while core inflation stayed more contained, underscoring the difference between temporary price spikes and underlying pressure.

- A new Federal Reserve regime under Kevin Warsh, with less forward guidance and a more hawkish tone, has made the policy path and reaction function more uncertain for fixed-income investors.

- Rising long-end yields and the return of term premium mean investors now need greater compensation for holding duration, making careful, risk-aware positioning across the curve more important than ever.

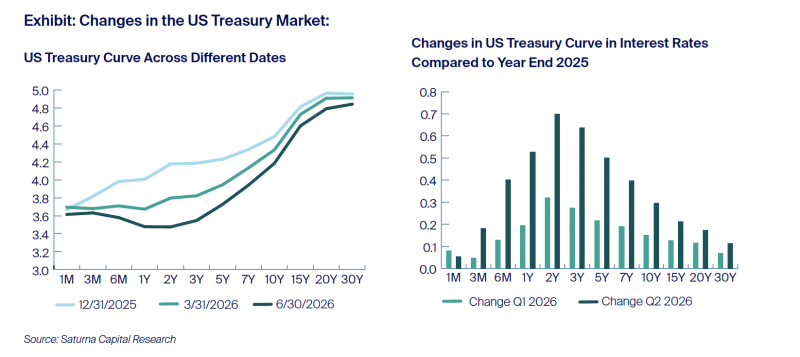

The second quarter of 2026 was shaped by three key developments: renewed supply-driven inflation linked to disruptions in the Strait of Hormuz amid the Middle East conflict; the appointment of Kevin Warsh as Federal Reserve Chair and the resulting uncertainty surrounding the policy path; and a broader rise in long-term yields as investors demanded greater compensation for duration risk. Together, these forces reversed the early-year narrative, in which investors broadly expected the Federal Reserve to shift toward easier policy.

Supply-led inflation and energy shock

The first key theme was the return of inflation pressure driven by supply disruptions. US headline consumer price index (CPI) increased 3.8% year over year in April and accelerated further to 4.2% in May, marking the highest annual reading since April 2023. The May data indicated that energy was the primary driver, with the energy index rising 3.9% month over month and 23.5% over the prior 12 months. Gasoline prices increased 7.0% month over month and 40.5% year over year. However, the impact of energy’s sharp inflation was partially mitigated by its relatively small 3.0% weighting in the CPI index. In contrast, larger index components such as shelter—which represents roughly one-third of the CPI basket—remained more stable, rising 0.3% month over month and 3.4% year over year. Core CPI, which excludes food and energy, increased a more moderate 2.9% over the prior year. For bond markets, that distinction matters: supply-led inflation may prove transitory if energy markets normalize, but it still lifts headline inflation, tighten financial conditions, and push nominal yields higher as investors demand protection against near-term inflation uncertainty.

New Fed Chair, strong data, and a less transparent reaction function

The second key theme was the arrival of Kevin Warsh and the uncertainty surrounding the Federal Reserve’s reaction function under new leadership. At the June 2026 meeting, the Federal Open Market Committee (FOMC) kept the federal funds target range unchanged at 3.50% to 3.75%, but the tone of the meeting was notably more hawkish than markets had expected. The FOMC said inflation remained elevated relative to its two percent goal, in part because of supply shocks that had driven price increases in sectors including energy.

That hawkish assessment was supported by the strong May employment report, which further constrained Warsh’s policy options. Total nonfarm payrolls increased by 172,000 in May, while the unemployment rate held steady at 4.3%. The result was significantly stronger than expected and more than double several pre-release estimates, reinforcing the view that labor market conditions remained resilient. Rather than inheriting an environment conducive to straightforward rate cuts, Warsh entered office facing firmer inflation and a labor market that continued to demonstrate sufficient strength to keep the case for easing on hold.

Uncertainty surrounding the FOMC’s policy path was further exacerbated by changes associated with Warsh’s appointment, which aim to reshape the Federal Reserve’s culture, communication, and policy assessment framework. The June statement removed forward guidance, and public reporting indicated that Warsh views such guidance as ill-suited to the current environment. He also announced five task forces to review communications, the balance sheet, data, productivity and labor markets, and inflation— signaling a broader reassessment of how the institution conducts and communicates monetary policy. Updated projections showed that nine policymakers now anticipate at least one rate hike by the end of 2026, underscoring how far expectations have shifted since the start of the year.

For fixed income investors, this combination of firmer inflation, stronger labor data, and reduced policy transparency increases uncertainty around the Fed’s reaction function and heightens market sensitivity to each CPI and payroll release.

Higher long-end risk premium and global rates

The third key theme was the rise in long-end yields and the return of term premium as a major driver of bond-market performance. Higher yields this quarter were not solely a response to stronger headline inflation; they also reflected a reassessment of the compensation required to hold duration in an environment of persistent inflation uncertainty, tighter financial conditions, and less explicit central-bank guidance. Even if the current inflation impulse ultimately proves temporary, longer-dated bonds can remain under pressure if investors conclude that central banks will be slower to ease and less predictable in signaling future moves. In practical terms, this means supply-led inflation and higher long-term interest rates should not be treated as identical developments: the former may fade if energy markets stabilize, while the latter can persist if investors continue to demand a structurally higher premium for duration risk.

For fixed income investors, the second quarter reinforced the need to separate front-end policy risk from long-end duration risk. The front end remains driven by incoming inflation and labor-market data and by the Fed’s evolving framework under Chair Warsh, while the long end increasingly reflects higher term premium and uncertainty about the long-run inflation and policy outlook. Against that backdrop, caution on duration remains warranted even if some of the recent inflation pressure fades in coming months. Higher all-in yields are improving carry, but the path for bond markets is likely to remain volatile until inflation moves lower more convincingly and the market gains greater confidence in the Fed’s framework.

In a fixed‑income market shaped by supply‑driven inflation, changing Fed policy, and higher term premiums, investors face greater uncertainty around both income and principal preservation. Our strategies aim to manage these risks through disciplined credit research, cautious duration positioning, and diversified portfolios that seek resilient cash flows and attractive valuations. For investors looking to capture today’s higher yields without taking uncompensated risk, partnering with an experienced, risk‑aware fixed‑income manager can help turn near‑term volatility into long‑term opportunity.