Fixed Income Markets Q2 2025 Commentary

Key Market Takeaways

- Perception shapes our understanding of events, but geopolitical tensions do not always directly impact financial market performance in the expected way.

- Despite escalating geopolitical conflicts, global fixed income markets have shown declining yields, signaling greater financial stability rather than disruption.

- The divergence between news headlines and market data underscores the importance of maintaining a long-term investment approach focused on time in the market rather than attempting to time market reactions.

Perception is powerful because it shapes the narratives we construct about both the world and ourselves. Given perception’s profound influence, it becomes crucial to examine the lens through which we base expectations, as one situation’s context doesn’t always align with another’s.

A compelling example of this can be observed in the contrasting trajectories between geopolitical news headlines and the performance of financial markets, often moving in seemingly opposite directions despite their interconnected nature.

The constant streaming of headline stories across news media outlets covering escalating geopolitical tensions in the Middle East and the ongoing Russian-Ukraine conflict has become inescapable. These human tragedies are both deeply real and profoundly difficult to witness. Such attention-grabbing coverage might lead one to assume that financial markets must also be experiencing similar disruptions, if not outright chaos. However, if one were to reverse this approach by examining financial markets first, the data would suggest that all appears well in the global economy — perhaps even optimistically so.

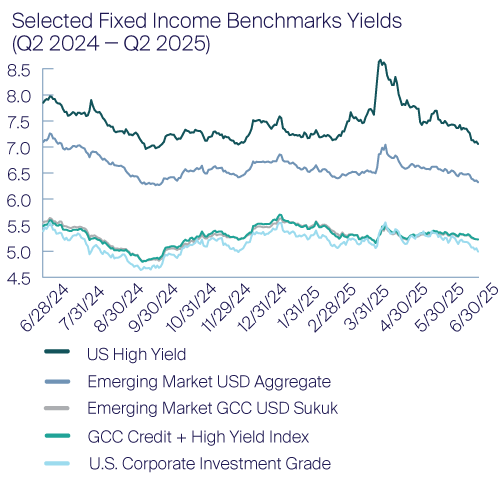

The accompanying chart offers valuable insight into trends across global fixed income benchmarks. The selected fixed income bond indices — including US-dollar sukuk, which predominantly originate from the Middle East — demonstrate that yields (or profit rates in the case of sukuk) have been declining progressively since early April. This trend coincides with the Trump Administration’s announcement of wide-scale tariffs on Liberation Day, April 2, 2025.

This trend can be observed in the Bloomberg US High Yield Index, which reached an apex yield exceeding 8.5% in early April and has since been trending relentlessly downward toward 7.0%. US-dollar sukuk, which predominantly originate from the Middle East, have exhibited a similar trajectory, with profit rates initially rising toward the mid-5.0% range before subsequently declining back toward 5.0%.

This pattern illustrates two important market dynamics. During periods of economic and financial disruption, yields rise to compensate investors for heightened uncertainty and elevated risks. Conversely, declining yields indicate that financial markets are operating in an environment of greater stability and certainty.

The key takeaway is incidents and news surrounding geopolitical events do not necessarily translate into similar outcomes within financial markets. If anything, this analysis reinforces the wisdom of the old investment adage: time in the market, rather than timing the market, is what matters most for long-term success.

As geopolitical and market-related events unfold, we will continue to employ conservatism and prudence to achieve the investment objectives of the funds, capital preservation and current income.