Equity Markets Q3 2025 Commentary

Key Market Takeaways

- Global equity markets delivered strong third quarter gains despite seasonal historical trends, with Japan and emerging markets leading performance and broad-based sector strength in the US, driven primarily by technology and AI-related companies.

- The rapid buildout of AI infrastructure, fueled by large strategic and “circular” investments among tech giants, raises concerns over sustainability, power supply constraints, and the uncertain ability of businesses to generate meaningful returns from AI initiatives.

- Political risks may heighten recession concerns, while the debt ceiling and tariff issues could further complicate the Federal Reserve’s balancing act between growth and inflation.

Contrary to popular market sayings such as, sell in May and go away, the third quarter proved a rewarding one for global stock investors. In the US, the S&P 500 Index returned 8.64%. Even September — historically the worst month for stock market returns and the only month to suffer an average negative return since 1950 — registered respectable gains with the S&P 500 Index appreciating 3.56%. During the quarter Japan and emerging markets performed best, followed by the US and Europe.

In the US, performance was broad-based as 10 of the 11 S&P 500 Index sectors registered positive returns, with Consumer Staples the lone outlier. To nobody’s surprise, Technology led all sectors followed by Communications, largely due to artificial intelligence (AI) adjacent Alphabet, and Consumer Discretionary, led by Tesla, which is as much a technology company as anything.

Technology received a boost when Oracle announced a huge new contract that sent the shares soaring 36.9% on September 10. When the major client was revealed to be OpenAI, questions immediately arose as to how it would fund future purchases from Oracle. In short order, Nvidia announced an investment, or “strategic partnership,” with OpenAI worth $100 billion. Such “circular” investments raise questions concerning the sustainability of the AI buildout. Nvidia invests $100 billion in OpenAI so OpenAI can purchase Nvidia chips to build out its large language models.

Nvidia also owns stakes in CoreWeave — which purchases Nvidia chips, installs them in data centers, then leases the data centers — as well as in datacenter operators Applied Digital and Nebius. Of course, Microsoft originated the practice when its investments in OpenAI were partially in the form of tokens or Azure cloud compute credits. When utilized, those credits were counted as revenue by Microsoft.

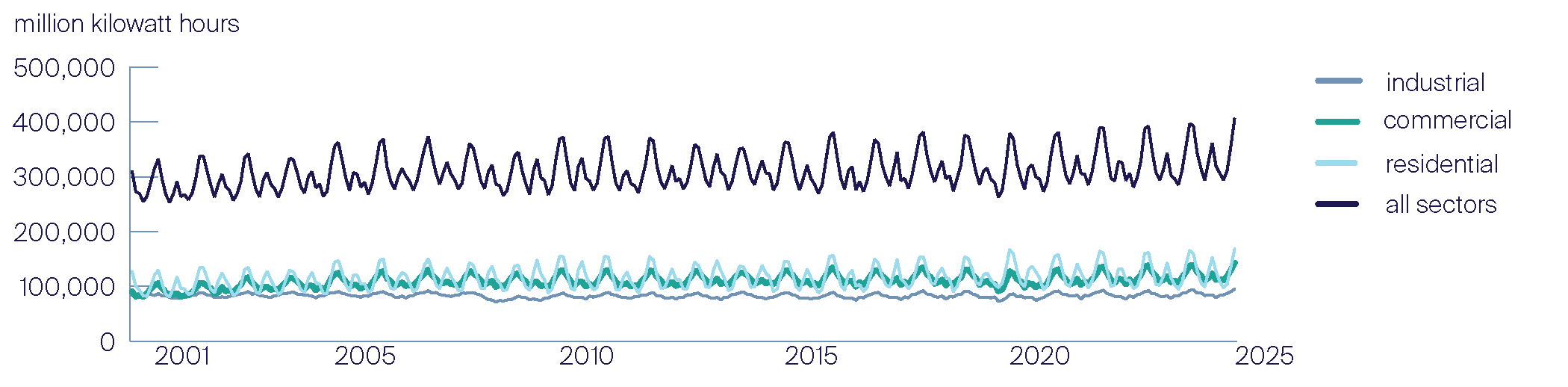

Power generation represents another issue facing AI development. After years of flat demand until around 2020, electricity consumption has been growing at a roughly 2% annualized rate. As the importance of AI inference (answering questions or performing tasks) grows relative to training, demand will increase further but it’s difficult to know how much. Utilities are overwhelmed with requests for connection to the grid, but how many of the requests are being submitted to multiple utilities? Utility companies are wary or overbuilding, being stuck with excess capacity and needing to raise customer rates. Of course, building new power infrastructure, especially grid improvements, is a time-consuming process made more difficult by the fragmented electricity market in the US.

Finally, we arrive at most important question: Will companies investing in AI ever see a return on their investments? The question concerns not only the companies building AI systems but also the companies hoping to leverage AI to improve their operations. Indeed, if the latter cannot make it work, the former will be hung out to dry. Nvidia, the Levi Strauss of AI, has already made its return but how many AI prospectors will find gold?

A July report by the Massachusetts Institute of Technology raises concerns. The report, titled “The State of AI in Business 2025” states, “Despite $30-$40 billion in enterprise investment into GenAI, this report uncovers a surprising result in that 95% of organizations are getting zero return.” Early days, to be sure, and much of the problem appears to stem from companies not understanding how best to deploy AI as much as the shortcomings of AI itself. Regardless, learning will take time while data centers and graphics chips are rapidly depreciating assets.

As the DeepSeek saga earlier in the year demonstrated, AI investment sentiment can turn quickly. More likely than not development will follow a similar trajectory to what was experienced with railroads in the 1800s, radio and the auto industry in the 1920s, and the internet at the turn of century. Stanford computer scientist Roy Amara said in the 1960s, “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.” AI may be another example of a well-established phenomenon.

Retail sales of electricity, United States, monthly

Market Outlook

September stands as the worst performing month historically but, courtesy of 1929 and 1987, October gets all the glory. This year it will be remembered for kicking off another government shutdown. Republicans and Democrats appear far apart on key elements of funding the government, especially relating to health care. We would not be surprised were the current impasse to break the 35-day record set in 2018 over disagreement on funding a border wall. Unlike a wall, which the Republicans eventually abandoned, the GOP is hanging its hat on reducing government spending, while the Democratic Party views healthcare as a core issue and an opportunity to drive a wedge between voters and Republicans. Neither side appears open to compromise. On the other hand, the shutdown may be over by the time you read this.

Interestingly, the stock market does not always react to disruptive events, including government shutdowns, Equity Markets Commentary in a manner one might expect. While the S&P 500 Index sunk 2.6% on the first trading day following the 2018 shutdown, it subsequently rallied over 13% by the time the government reopened. That may have had to do with the nature of the dispute, which did not include raising the debt ceiling. Investors have remained remarkably sanguine regarding the vast increase in debt over the past several years, but debt ceiling fights have the effect of bringing the issue into focus.

Conversely, President Trump has indicated that he will approach the shutdown differently than past administrations. Rather than striving to keep as many services as possible operating, furloughing workers or asking employees to work without pay, the administration plans to engage in aggressive layoffs – a throwback to Elon Musk and the days of DOGE. Just like DOGE, it’s likely many of those employees would eventually be recalled when the necessity of their work becomes apparent. In the meantime, however, recession fears may rise at the same time tariffs are expected to exert a greater influence on inflation, exacerbating the growth versus inflation conundrum faced by the Federal Reserve.

About the Author

Important Disclaimers and Disclosures

This publication should not be considered investment, legal, accounting, or tax advice, or a representation that any investment or strategy is suitable or appropriate to a particular investor’s circumstances or otherwise constitutes a personal recommendation to any investor. This material does not form an adequate basis for any investment decision by any reader and Saturna may not have taken any steps to ensure that the securities referred to in this publication are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the publication. The information in this publication was obtained from sources Saturna believes to be reliable and accurate at the time of publication. All material presented in this publication, unless specifically indicated otherwise, is under copyright to Saturna. No part of this publication may be altered in any way, copied, or distributed