A More Constructive Economy, a More Fragile Market

Key Market Takeaways

- The energy and geopolitical tail risk that defined the first half faded without transmitting to an inflation surprise, and equities rallied. But market leadership narrowed sharply to artificial intelligence and megacap names, leaving a more constructive economy paired with a more fragile market.

- The AI debate flipped from a fear of over-investment to a fear that the industry was under-investing to keep up with surging demand. That swing powered the rally, even as questions emerged about how durable that demand really is, while a wave of very large AI-related IPOs began to arrive that will further test investor appetite.

- In a narrow, concentrated market, we continue to favor resilient, well-governed companies with durable franchises and strong balance sheets, and we view our screening discipline as a source of resilience rather than a limitation.

The second quarter of 2026 was not an all-clear so much as a rotation in the source of risk. The downside scenarios that dominated at the beginning of the second quarter — continuation or escalation of the Iran war, indefinite closure of the Strait of Hormuz, and an energy-driven inflation shock — appear on their way to being resolved. As those tail risks faded, equities rallied sharply. But the source of strength also narrowed: the rally increasingly rested on expectations for artificial intelligence (AI) demand growth, and the durability of that growth became the central question.

Read against last quarter, the two risks we flagged receded in tandem. The energy shock receded, and the fear that the industry was over-investing in AI flipped into a fear that it was under-investing. Both developments favored equities. What replaced these risks is more subtle and easy to miss after a rally: risk did not recede so much as change form. The fading of macro-economic risk has given way to the risk of leaning on a single bet — the durability of AI demand — with a wave of new AI issues set to draw on the same pool of capital.

The shock that faded

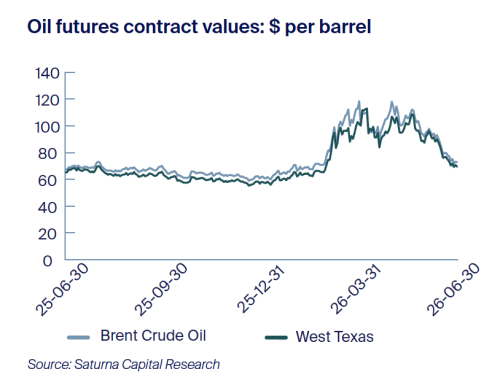

The central question entering the quarter was whether the energy shock would transmit into the real economy and reignite inflation. So far, it has not. Physical disruptions eased, inventories and strategic petroleum reserve releases cushioned supply, and oil prices retreated as the risk of a sustained Hormuz closure faded, with Brent Crude Oil falling roughly 25% in June.

When hostilities escalated, oil, energy equities, agricultural materials, and defensive industries outperformed, while traditional hedges proved less effective as Treasuries and gold sold off alongside long-duration growth and international equities. When tensions calmed, these threads just as quickly unwound — round-tripped lower, defensives gave back relative ground, and leadership rotated back to growth and AI, led by semiconductors, which posted their best quarter on record (dating to 1994).

The AI tug-of-war

Within the AI trade itself, a genuine tug-of-war took hold. The initial AI-driven rally appeared to be driven by a swing from a fear of over-investment to a fear of under-investment, and that swing did much of the work in lifting chips, hyperscalers, and even memory. OpenAI’s willingness to strike creative, long-dated deals that hand compute providers equity upside began to look prescient, while Anthropic strained to keep pace with extraordinary demand for its models and for applications such as Claude Code and Cowork. Both companies reported rates of revenue growth almost unheard of at their scale, and the market read the binding constraint as capacity, not demand.

As that narrative took hold, a more sober question surfaced: how much of the demand is durable. At least some of the growth appears to reflect usage incentives — “token-maxing” among the largest users — rather than clearly value-producing activity. The tension is unresolved, and both sides may hold a piece of the truth. The heaviest AI users today are concentrated in coding, and if their token-maxing has been inflating the very revenue-growth figures that convinced the market demand was outrunning supply, then a great deal now rides on demand broadening beyond code. Until that broader adoption is proven, the AI demand growth powering the rally rests on a possibly overstated base.

A wave of new issues, and our core investment discipline

We noted last quarter that the largest private AI companies would eventually need public capital. That need has arrived. SpaceX completed its recordbreaking IPO — buoyed by its growing ambitions of hosting AI compute beyond terrestrial data centers — while OpenAI, and Anthropic have formally begun the process of preparing their public offerings, both expected later this year. This is a new supply of very large, AI-related equity that could absorb meaningful investor capital.

We have been asked frequently about the SpaceX offering. Our rationale for avoiding investment there is illustrative of our investment philosophy and process: governance concentrated overwhelmingly in a single insider, with limited protections for outside shareholders; a business mix — including defense activities and an affiliated content platform — that does not fit our values screens; and a company years away from profitability at a valuation that leaves little room for error. Governance and business quality are not considerations we brush aside when frenzy takes hold. They are the screen.

Outlook

We expect AI and geopolitics to remain the dominant forces through the balance of the year. The buildout is likely to continue even as its economics stay unsettled, and the range of winners and losers may continue to widen. A pipeline of large new issues will test the market’s appetite, and the current macro calm is contingent rather than guaranteed.

Our investment philosophy involves adherence to a values-driven process that is durable to a range of outcomes. Resilient, high-quality companies with low debt have adaptability to themselves navigate a wide range of environments. Our values discipline is not a constraint but an expression of this resilience across our various strategies. A more fragile market is precisely where we expect our approach to earn its keep.